Publisher-Exchanges: Consumer Applications and the Attention Theory of Value

“The price is the news” is an often used adage in crypto circles any time there is heightened engagement and awareness around a network following fast price action. It has become clear to me that the inverse of this statement is perhaps more profoundly true: “The news is the price.”

In my contribution to What Multicoin is Excited About For 2024, I described a marked shift in how markets price assets that I labeled the “Attention Theory of Value.” In crypto, the primary input into asset pricing is not multi-factor models around risk premiums or cashflows, but rather the perceived amount of time, energy, and money that a community around an asset devotes to it. Note that this is not a normative statement, but rather an observation of capital flows over the history of tokens as an asset class (see recent memecoin flows as an early instantiation of this).

The internet enabled arbitrary, bi-directional information transfer. Crypto builds on top of those rails by enabling arbitrary, bi-directional value transfer. The consumer internet today—streaming platforms, online media, mobile apps, social media, etc.— can be summarized as a marketplace for attention, and as such, money and attention increasingly share similar characteristics.

In the 1930s, Benjamin Graham would have to wait for quarterly reports and financial statements to express his value investing thesis by purchasing paper stock certificates via a human broker. In the 2020s, a series of Reddit posts about short-selling activity from hedge funds on Gamestop drove tens of thousands of retail traders to submit buy orders on Robinhood, driving the price up 15x over the course of thirty days. The consumer internet and crypto rails make the atomic units of information and value drastically smaller, and simultaneously increase the volume and frequency of both data consumed and value traded. As this happens, the attention theory of value becomes tighter — information is money, and money is information.

While marketplaces for both attention and value exist in the wild, we have yet to see them truly collide. When we think about consumer apps in crypto, this is what we are looking for. Crypto enables the ability to quickly create new assets around attention, and the ability to trade them where that attention is aggregated: consumer-facing applications.

In coming years, we expect consumer developers to meaningfully incorporate crypto into the fabric and user experience of their apps, massively shifting the overton window for what can be traded and where. Internally, we’re calling this class of apps “Publisher-Exchanges.”

Publisher-Exchanges

Exchanges naturally have product-market fit in crypto because one of the core uses of crypto is to move value around. Coinbase (fiat on/off ramp and centralized exchange), Tensor (an exchange for digital collectibles), Jito (an exchange for transaction intent and blockspace), and Phantom (an exchange for taker orderflow) are all exchanges of different forms.

Exchanges are to crypto what major publishers (e.g., X, Instagram, and The New York Times) are to the consumer internet: publishers control the flow of attention in the consumer internet, and exchanges control the flow of money in crypto.

As we think of the next generation of consumer applications, we expect to blur the lines between exchange and a publisher, forging new experiences that combine money and attention.

Kyle wrote about UI layer composability for his 2024 ideas contribution. The simplified implication of this thesis is that the next big online exchange will not look like Coinbase with a traditional orderbook, depth chart, etc.; instead, it will look like a short-form video app where audiences can wager on the virality of upcoming creators’ content, or a group chat where friends can instantly launch an NFT collection based on an inside joke or meme, or an are.na-style curation platform where designers are rewarded for their taste in both status and money. In other words, consumer applications that are uniquely enabled by crypto are both publishers and exchanges: publisher-exchanges.

Publisher-exchanges increase the surface area for new asset issuance by embedding issuance and native trading into application front ends, and allow for novel ways to interact and coordinate those assets. The introduction of trading into familiar venues may seem narrow or skeuomorphic, but we believe narrow markets are the wedge for discovering emergent behavior, which leads to the creation of massive new platforms.

This will be a golden era of experimentation— a blank state for developers to run experiments that combine native issuance and trading with novel in-app experiences. ”Crypto-native consumer applications” will treat these design principles as a first class citizen.

Emergent Categories of Publisher-Exchanges

The north-star for Publisher-Exchanges is to facilitate the applicable version of trading alongside what has a user’s attention at any given moment in time. The next generation of consumer applications in crypto will allow their users to issue and trade assets natively, thereby monetizing the user attention they capture directly.

For founders looking to build Publisher-Exchanges, we believe a few design principles from the histories of both publishers and exchanges will be relevant.

In the history of the consumer internet, publishers are inherently content marketplaces, and marketplaces are fueled by two core properties: 1) discovery and curation (presenting things that users want to see and interact with), and 2) trust and reputation (providing assurances to users). Successful publishers can generate a strong “liquidity” by measuring the attention users spend on them. This is why Upworthy measured success in “attention minutes” and why Elon Musk is obsessed with “unregretted user minutes” and “user seconds.”

The takeaways here for publisher-exchanges are that they first need to build engaging core experiences that draw time and commitment from their users, and next embed asset issuance and transfers that map cogently to the unique style of engagement they generate.

We don't think of exchanges as a simple trading venue, but rather an Athenian agora where people interact and exchange experiences, value and information in a tightly defined, context specific environment. With that in mind, we’ve dreamed up a few broad categories of applications we think are ripe for Publisher-Exchanges to emerge.

MESSENGERS

Chat applications are prime candidates to be Publisher-Exchanges.

An early illustration of this thesis is apparent in WhatsApp and WeChat. Both platforms boast rich developer ecosystems in India and China and are built atop robust, state-mandated digital payment rails. This allows teams like Sama and Meesho to embed labor markets for AI labeling and local merchant ecommerce directly into the contextual state that exists within users’ social graphs on these platforms.

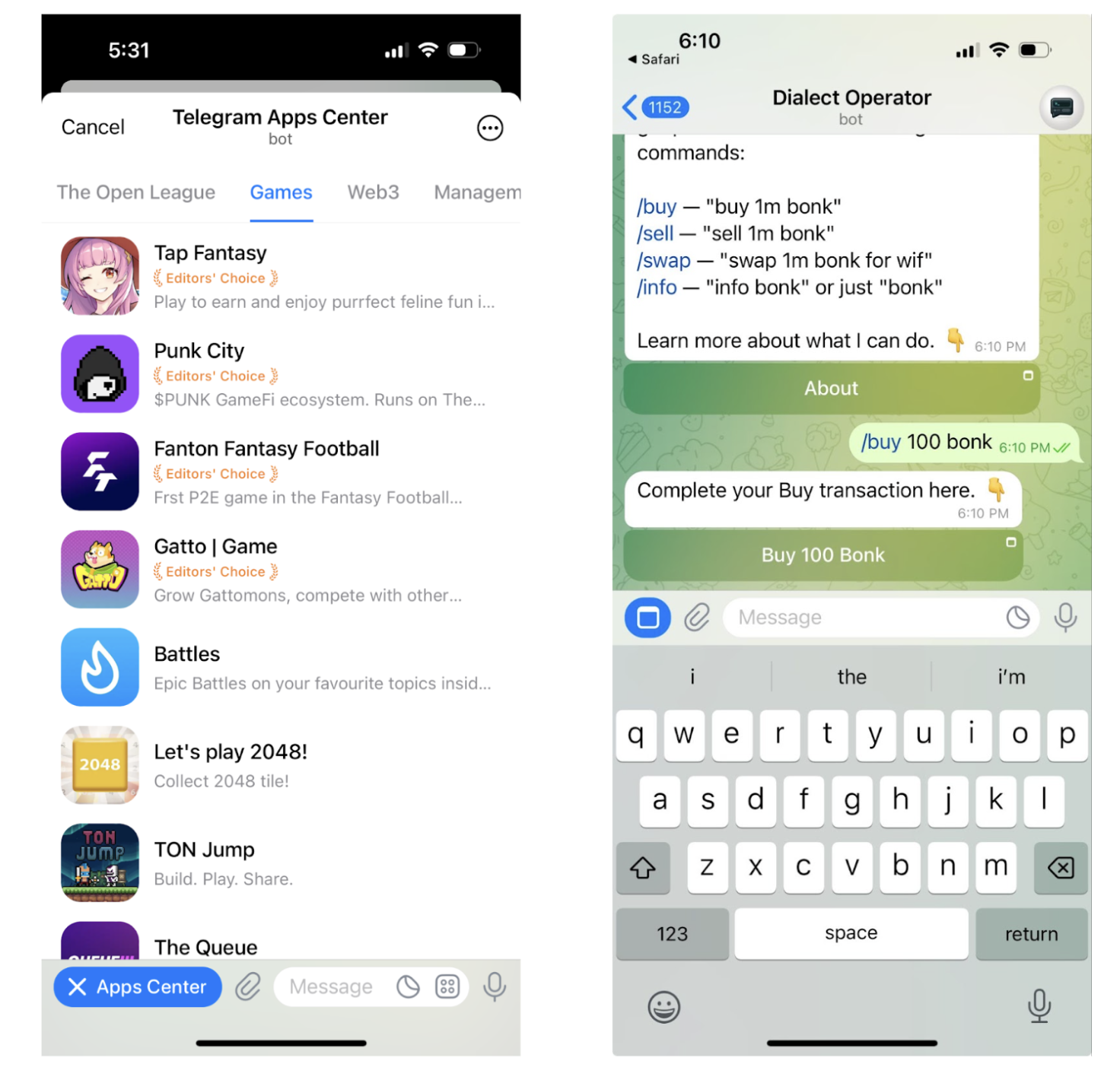

Within crypto, Telegram is the de facto messenger, and their bot API creates a vast design space to embed issuance and value exchange experiences. Products like Dialect Operator and Maestro are examples of this in the wild. They are evidence that users want to be able to place trades directly within their chats. These Telegram trading bots fit the definition of Publisher-Exchanges because they bundle discovery and intent with execution, tightening the loop between attention and value transfer. Telegram has its own hidden app store (go to search, then type ‘tapps’) with hundreds of bots that allow users to send payments, play games, discover content, and more.

While these Publisher-Exchange bots are used to reduce time to execution for retail traders seeking alpha in closed chat groups, there are further opportunities to massively increase the set of assets that can be issued and traded. We expect chat groups to be a base layer for new forms of work (get paid for completing a task directly in chat), special projects (crowdfund new initiatives inside large conversations), and play (issue memecoins as easily as sending a gif)—all of which are Publisher-Exchange experiences.

CONTENT NETWORKS

The largest social media applications (Instagram, TikTok, X, Youtube) are content marketplaces, wherein the creators of music, posts, videos, or other user-generated content compete for users’ attention. Creators can then use the attention they accumulate to sell content or branded products.

The north star for crypto content networks has been audiences backing individual creators or pieces of content, and creators receiving a major share of the upside in the content they create. This was the original thesis for creator tokens, but we learned that creator tokens alone are unlikely to succeed if they are disconnected from the platforms on which their audiences reside.

We are seeing early experiments in novel content networks today, each with new types of assets issued and traded in-app. We envision a new type of content marketplace in which users come for entertainment and stay for the market.

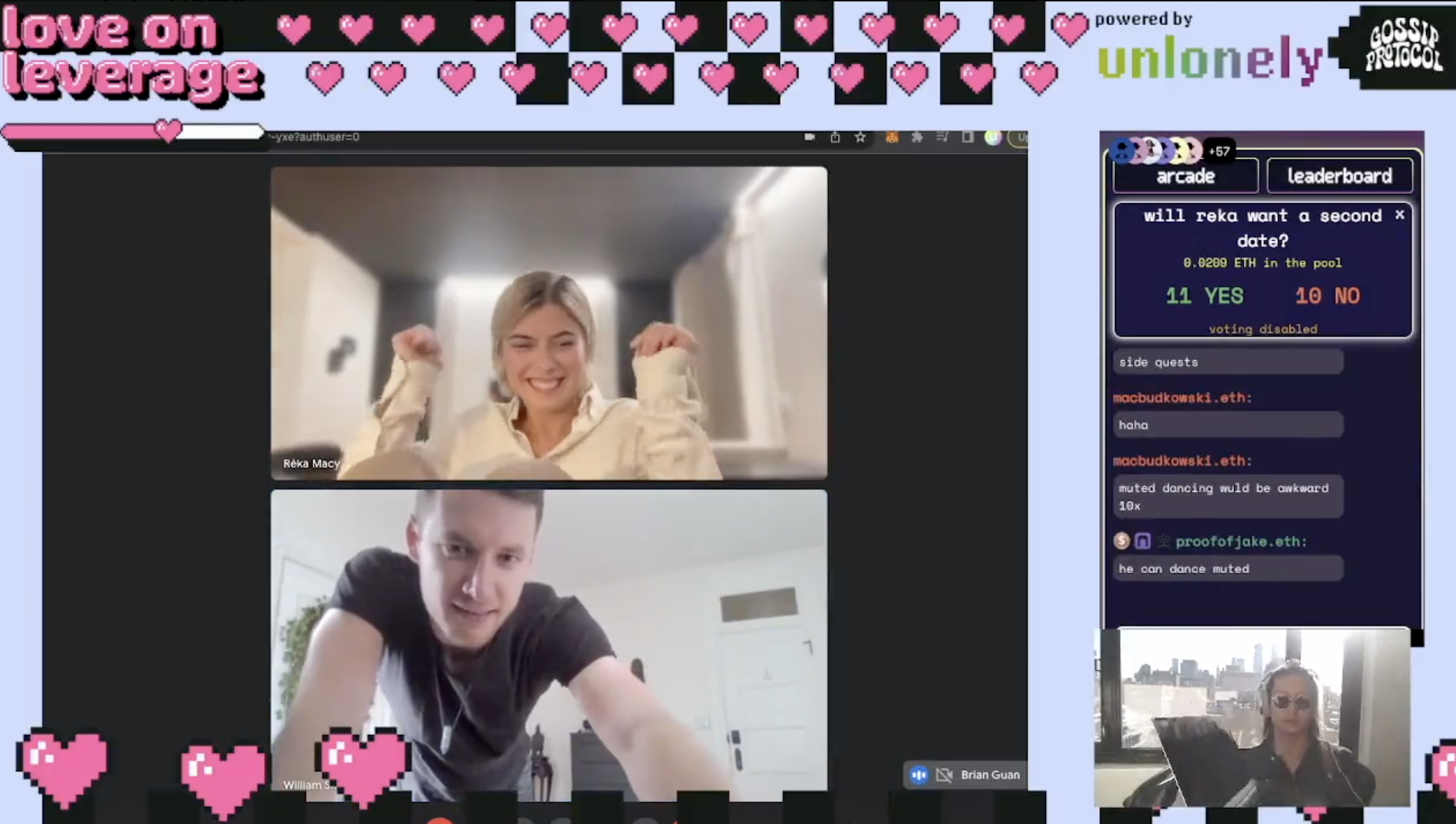

Unlonely is a streaming platform that embeds token issuance and prediction games directly into streams and chats. Farcaster Frames, which enable direct, in-feed interaction with onchain state, are another example that enables endless opportunities to issue and trade assets in a familiar venue.

Most content networks today monetize attention through display advertising. The ad-based model of customer acquisition typically has a leaky conversion funnel, and is explicitly a sub-par solution to capture attention because it often interrupts the user experience; users are aware that they are being marketed to.

Display ads are a relic of the pre-crypto era. A more first-principles approach for merchants to acquire users is through Direct Value Issuance (DVI) — i.e., directly pay users with tokens.

Instead of delivering targeted ads based on user behavior/cohort construction, advertisers should be able to distribute value to users directly. A content network does not need to place an ad for a sports betting platform between posts a user is scrolling around an NBA game that is live — it can, instead, allow the sports betting platform to directly airdrop $50 worth of credit to the user for the platform.

Advertisers, insteading of transacting with platforms as rent-seeking intermediaries, deliver their CAC budgets directly to end users. In turn, content marketplaces can offer a superior product to their users: they transition from being venues in which users are actively being farmed for their attention and seeing none of the upside that results from the financialization of that attention (via display ads), to giving them direct exposure to that financialization via earning and spending assets based on their attention patterns (via DVI).

The backdoor embedded ad networks opens is perhaps far more compelling — by providing every user with an address, it makes it possible for applications to embed general purpose financial services at zero cost, which can be layered on top of the deep contextual state that already exists amongst its users.

INFORMATION MARKETS

Search engines in the 90’s sought to organize the information on the internet, focusing on static web pages at first and then expanding to new forms of media and content. The cost of accessing this information was subsidized via ads.

Today, information on the internet is much broader than webpages — it lives across thousands of forum threads, group chats, podcasts, and private databases. Information markets (e.g., prediction marketplaces, sports betting platforms, alternative data providers) are a way for users to directly isolate signal from noise across all of these sources, and distill the probability of an outcome from large swaths of qualitative information.

While the most successful instantiations of information markets do not presently rely on crypto rails, we believe that they can be supercharged by crypto primitives. The design space here is either financializing the information itself based on quality, or embedding these markets directly into the venues where first-party information gets shared.

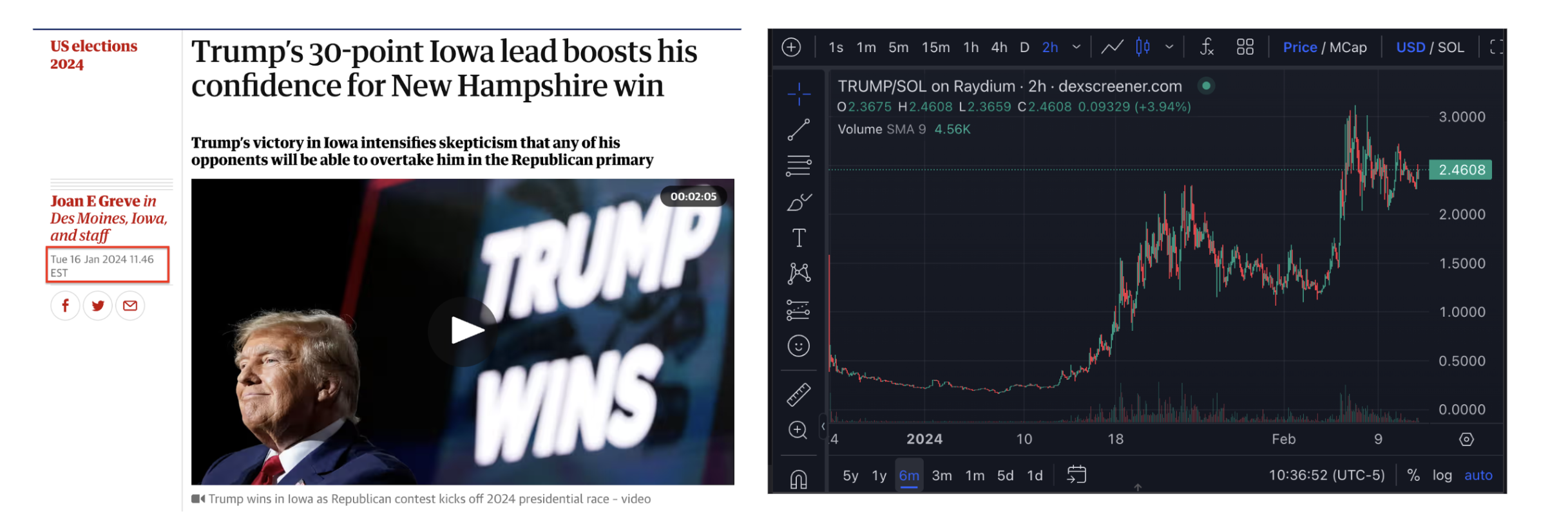

Prediction markets like Polymarket are effectively binary call options with expiries around future outcomes like elections or sports events. Historically, they have failed to accrue enough liquidity or attention required to act as reliable information sources. In contrast, cultural spot assets (memecoins or NFTs) have proven to be a higher signal for attention (and information) than siloed prediction markets, because they don’t have fixed expiries and can take on a life of their own. For instance, Trump associated NFTs and tokens consistently trade higher volumes than Polymarket prediction markets.

As such, new spot assets that directly track attention could represent a more interesting proxy for attention or information flows. Embedding these types of assets into news distribution platforms or editorial publishers could allow for a more compelling construction than the binary, fixed-expiry constructions of the past. In the same way that Numerai borrowed from the principles of token-curated registries to run machine learning competitions over obfuscated financial data, we believe there are general information markets that can be built for new categories of information along the same principles.

Consider a StackExchange-style forum where votes and reputation primitives carry financial value, or a Pinterest-style curation board in which users can stake their reputation on emergent trends and behaviors. There are massive quantities of high quality information on the internet today, mostly contributed by users for no financial incentive whatsoever — what is missing is the form factor to properly aggregate and monetize it, and that is where crypto primitives are most useful.

We are excited about new instantiations of this thesis, and in general, tokenizing the intangible quantities in content networks: accuracy, reputation, humor.

SPECIAL-INTEREST COMMUNITIES

Tokens allow communities to draw attention to novel problems, and steward resources toward them. ConstitutionDAO demonstrated that a memecoin could pool together enough funds to bid on a rare artifact, and the network took a life of its own after the auction itself.

The takeaway in this instance is that tokens are more likely to coordinate real world action when there is a mission attached to them. This exact collaborative funding model could support new ventures that are traditionally ignored by conventional lines of funding and research: capital intensive projects like VR headsets, obscure corners of open source software, artistic spaces, or drug discovery for rare diseases.

Tokens uniquely enable capital formation from distributed sources, and give capital providers strong ownership rights around the products of that capital. This means that groups around the world can coordinate capital to run experiments at massive scale, productize the results of those experiments, and pass through earnings back to the token.

HairDAO and VitaDAO are examples of this in the wild today. We are already seeing new platforms for collaborative research, funded and sustained by the attention accrued around a variety of overlooked problems.

An Infinite Canvas For Trade

Consumer crypto applications will be a generative shift, not an imitative one. The primitives we have described in this piece demonstrate a tight loop between attention, capital formation, and coordination because the primary unlock for crypto is that trades can happen everywhere. Rather than just moving existing economies on-chain, crypto unlocks new economies for attention where like-minded cohorts of people can trade minutes for dollars and vice versa.

/The Holy Grail of Cryptography

Today, I’m excited to announce that Multicoin Capital has co-led a $73M investment in Zama, alongside Protocol Labs

Disclosure: Unless otherwise indicated, the views expressed in this post are solely those of the author(s) in their individual capacity and are not the views of Multicoin Capital Management, LLC or its affiliates (together with its affiliates, “Multicoin”). Certain information contained herein may have been obtained from third-party sources, including from portfolio companies of funds managed by Multicoin. Multicoin believes that the information provided is reliable and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post may contain links to third-party websites (“External Websites”). The existence of any such link does not constitute an endorsement of such websites, the content of the websites, or the operators of the websites.These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Websites. The content of such External Websites is developed and provided by others and Multicoin takes no responsibility for any content therein. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice. You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by venture funds managed by Multicoin is available here: https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced due to coordination with the development team(s) or issuer(s) on the timing and nature of public disclosure. Separately, for strategic reasons, Multicoin Capital’s hedge fund does not disclose positions in publicly traded digital assets.

This blog does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest.

Past performance does not guarantee future results. There can be no guarantee that any Multicoin investment vehicle’s investment objectives will be achieved, and the investment results may vary substantially from year to year or even from month to month. As a result, an investor could lose all or a substantial amount of its investment. Investments or products referenced in this blog may not be suitable for you or any other party. Valuations provided are based upon detailed assumptions at the time they are included in the post and such assumptions may no longer be relevant after the date of the post. Our target price or valuation and any base or bull-case scenarios which are relied upon to arrive at that target price or valuation may not be achieved.

Multicoin has established, maintains and enforces written policies and procedures reasonably designed to identify and effectively manage conflicts of interest related to its investment activities. For more important disclosures, please see the Disclosures and Terms of Use available at https://multicoin.capital/disclosures and https://multicoin.capital/terms.