What Multicoin Is Excited About For 2024

At the end of every year we come together and discuss some of the biggest changes we’re expecting in the year ahead. For the first time, we’re publishing these ideas. Please feel free to reach out to any of us to discuss these ideas further.

Shayon Sengupta

The Attention Theory of Value

Exchanges are used to trade things that are easy to price—stocks, commodities, interest rates, etc. There are canonical ways to measure these assets (e.g., some function of discounted future cashflows—DCFs—for stocks; the going rate for a barrel of oil at the border; the willingness to pay for $1.05 that can be redeemed in the future). This is what price discovery means for liquid markets.

However, there is a separate class of goods where price discovery occurs purely around attention. Sneakers, art, sports collectibles, vintage furniture—these are inherently less liquid than stocks or commodities, and their value comes purely from social consensus, not from a DCF model.

In recent years, and in large part due to the internet, The Attention Theory of Value has bled over to traditional markets. TSLA, GME, AMC, DOGE and CryptoKitties all underwent meaningful price discovery under this model. The primary pricing mechanism for these assets used to be cashflows and clearing prices but now the primary mechanism is derived from the amount of attention they receive.

Crypto plays two important roles in The Attention Theory of Value: the first is the ability to quickly create new assets, and the second is the ability to trade them. If attention is the core pricing factor, then what crypto enables is an infinite canvas to issue and trade assets that track attention. The broader pattern of “financializing attention” requires two of crypto’s most important properties to reach its natural end state: permissionlessness and composability.

- Permissionlessness: Anyone can issue assets of any kind

- Composability: Anyone can trade those assets on any venue

This design space for experimentation:

- Increases the surface area for new asset issuance (i.e., historically, creator tokens, prediction market LP positions, memecoins)

- Embeds issuance and trading into new venues (i.e., historically, messenger bots like bonkbot or bananagun, leaderboards like friend.tech, in-game marketplaces)

- Facilitates coordination among asset holders (i.e. historically, pool capital to purchase a copy of the constitution, build out radio footprint for carrier offload)

The near term implication of this is that the next big exchange will not look like an exchange. It will look like a livestreaming platform where creators and audiences bet alongside each other, or a group chat where friends and communities can instantly launch a crowdfunding campaign to raise millions of dollars to build out a network state, or a Stack Exchange-style forum where top contributors are rewarded for their contributions not only in platform-specific status points, but also in material financial upside.

In 2024, we'll see entrepreneurs run experiments along these three broad patterns. we'll see the first “non-exchange” exchange for both liquid and illiquid assets emerge. These exchanges will climb the leaderboard in terms of volume, and pick up where Wall Street Bets left off.

Vishal Kankani

Social Networks for NFT Collectors

In 2024, I’m excited about collectible NFTs, more people getting into collecting, and social experiences for collectors.

Collecting has ancient origins, from monarchs amassing unique treasures in Egyptian and Chinese civilizations to the Renaissance European cabinets of curiosities. Museums, in essence, evolved from these private collections.

Psychologically, beyond speculative opportunities, collecting serves as a means of self-expression. In certain circles, collections transform into status symbols, intertwining the act of collecting with personal identities, signifying commitment, expertise, and knowledge. The internet has amplified this behavior, connecting previously isolated enthusiasts and fostering a new sense of belonging in their respective tribes.

Despite this advancement, several barriers plague collectors:

- Fraud related to authenticity and provenance

- Trade and exchangeability

- Security, damage and loss

- Space and storage concerns

Blockchains, by definition, collapse the above barriers by orders of magnitude and attract more people to collect. Blockchains particularly appeal to younger generations who are already into collecting digital items—think Pokemon Go, virtual sneakers, and in-game skins. These collectibles were all precursors to digitally-native collectibles that reside on public blockchains.

Even if digital collectibles transition from private databases to public blockchains, a certain set of behaviors from collectors will remain constant: the desire to flaunt their collections, to exchange collectibles easily, to discover, to connect, and interact with their tribes. These behaviors will set the stage for the rise of social experiences based on ownership graphs.

Spencer Applebaum

Stablecoin-Powered Remittances in Emerging Markets

I fell down the crypto rabbit hole after interning at Bitspark, one of the first companies to use BTC as rails for remittances, primarily in SE Asia and Africa. Crypto-powered, cross-border payments is one of the use cases I’ve been most excited about since discovering crypto.

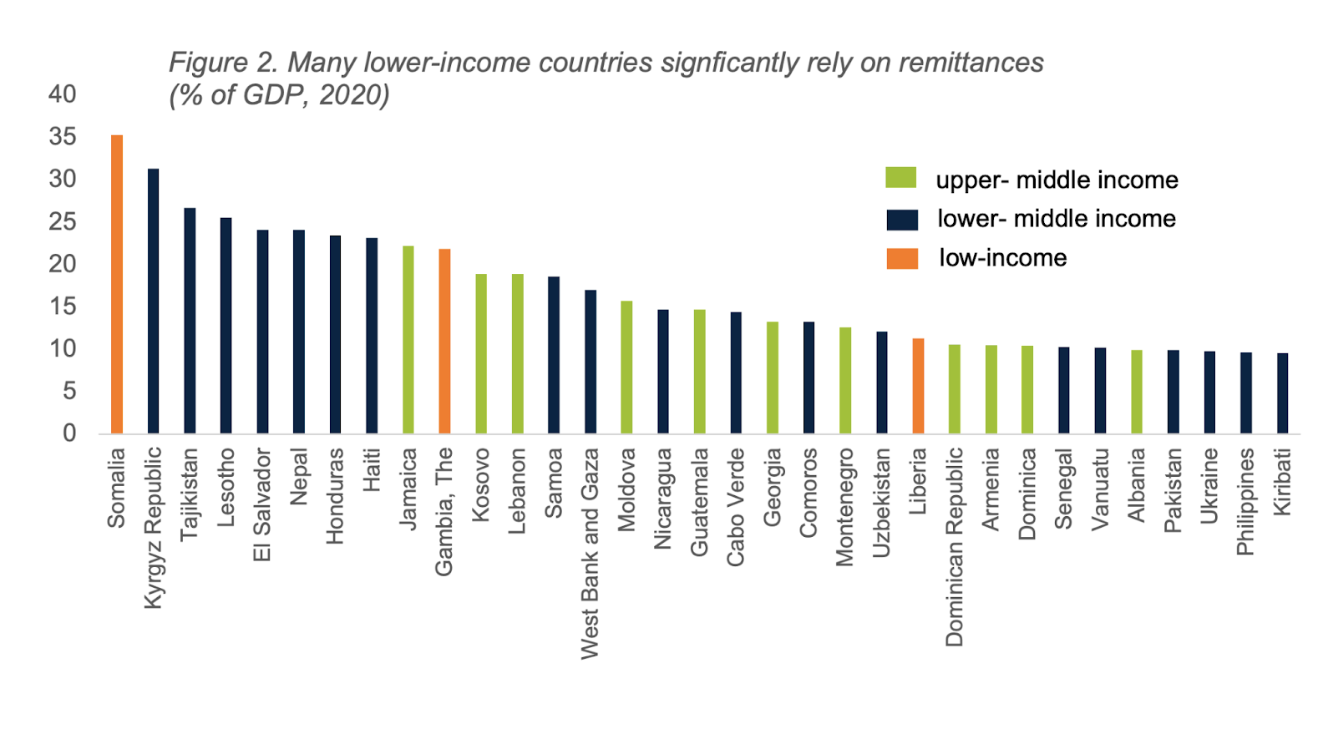

In some lower-income countries, the remittance industry is one of the biggest drivers of GDP, and is how many economies are able to sustain:

Source: Based on data from World Bank Development Indicators

Source: Based on data from World Bank Development Indicators

Historically, the challenge for remittances has been that costs are high, and only a very small number of fiat currencies are exchangeable and tradable outside their country of origin (e.g. USD, EUR, JPY, GBP), which makes many corridors slow and inaccessible. According to The World Bank, sending remittances costs ~6.2% on average, but that spread intuitively increases substantially for long tail exotic corridors. For example, sending money from South Africa to China costs over 25%(!).

With that context, I’m excited about the opportunity for both 1) consumer-facing remittance apps and 2) B2B SaaS companies for physical money transfer operators (MTOs)—specifically MTOs that utilize stablecoins in corridors that are traditionally inaccessible and/or expensive—to emerge in 2024.

These products 1) exchange local currency ABC for USDC/USDT in a P2P way (e.g., oRamp or El Dorado) via local payment methods, 2) send USDC to another country, and 3) either hold USDC or swap it out to local currency via familiar domestic payment methods with another broker or liquidity provider.

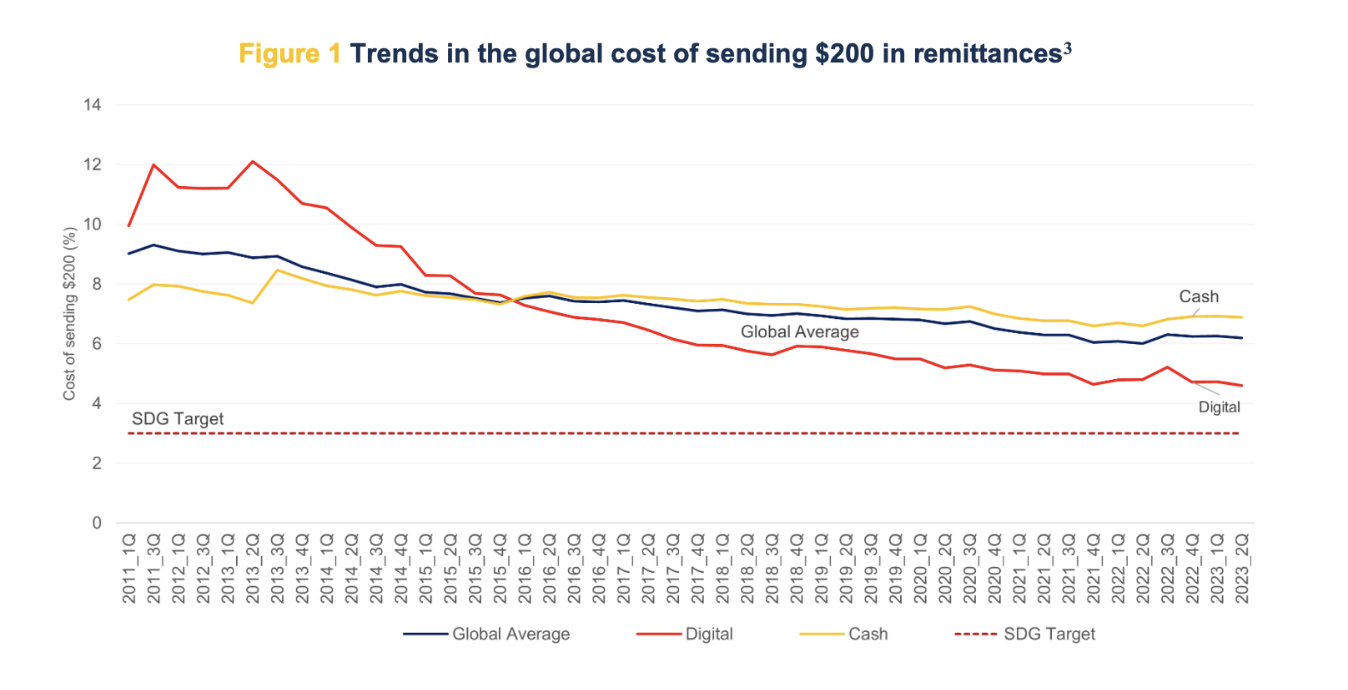

Digital payments have had a profound impact on global remittances over the last 12 years:

Source: World Bank Remittance Prices Worldwide Quarterly

Source: World Bank Remittance Prices Worldwide Quarterly

Stablecoins will accelerate this trend and reduce costs for remitting money even further, particularly in long-tail corridors that have historically been slow and expensive. With rapid stablecoin adoption in 2023, the year of stablecoin remittances will be 2024.

Matt Shapiro

Crypto Shifting From Being the Product to Powering the Product

In 2024, we will see a meaningful shift from crypto being the product, to crypto powering the product. The early signs of this are already happening today and I believe green shoots are abound.

Last year, crypto lit up novel marketplaces that historically have either been impossible or highly inefficient. Hivemapper created an entire new map that sees a location 24 to 100 times more frequently than Google Street View—and mapped nearly 10% of the earth in less than a year—using crypto-mechanics to incentivize permissionless contributions in a scalable way. During a world-wide GPU shortage, Render Network created an entirely new marketplace for GPU supply—an area that we believe will face continued supply/demand imbalance in the years to come. Helium Mobile is seeking to materially shift the cost structure of the telecom industry by piggybacking on crypto-enabled, user-owned infrastructure and equipment.

Nubank, one the largest neobanks with more than 80 million customers, is leaning into crypto with the launch of Nucoin as a form of loyalty. Starbucks is leaning into crypto with their Odyssey program, an offshoot of their existing top-tier rewards program. Blackbird is using crypto rewards as a wedge into restaurants (which can be a precursor to driving a robust payments business that adds additional margin to the bottom line of restaurants).

BAXUS is using crypto to light up a marketplace for trading and investing in whiskey and other fine spirits, opening the market to a new pool of participants. oRamp is using crypto to light up a new marketplace for local and regional foreign exchange, enabling tighter spreads and reduced costs for customers.

All of these examples are very different, but at their core they are the same: they are all using crypto to power products that drive a meaningful economic outcome. In some cases, like Starbucks, Nucoin, and Blackbird, crypto is mostly obfuscated and operating under the hood. In other cases, like Hivemapper and Render, crypto is tightly coupled, highly visible, and a key part of the product itself. The design space here is wide, and the infrastructure buildout over the last 5 years has paved the way for crypto to power everyday use cases. In 2024, experimentation in this arena will explode.

Eli Qian

On-Chain Data

In 2024 I expect the amount of on-chain data to grow by orders of magnitude. As new users are onboarded, the use cases and functionality of dApps and protocols will grow as well. Data from decentralized social protocols will be especially abundant—people do more things and produce more data on social products than financial products.

What will we do with this explosion of data? In the past, on-chain data has been viewed through the lens of advertising and personalization. However, I’m eager to see teams take a more first-principles approach and acknowledge that contextualizing on-chain data isn’t just a luxury, but a necessity when it comes to building social products.

Currently, our on-chain social data and identity is built into one, universal graph (e.g. Farcaster), making it difficult to build social products for different social contexts. People are multifaceted. We live across a wide range of social contexts. We act differently and require different things depending on the context. We go to Facebook, Twitter, LinkedIn, and Snapchat for unique reasons—the social graph creates a specific context and experience on each platform.

The launch of Threads offers a case study in this. There are many reasons why Threads did not kill Twitter, but one reason was the ambiguous social context. The social graph of Threads was imported from Instagram—a social network with context primarily tied to IRL relationships. But the medium of Threads, the ways users interacted, was taken from Twitter, an online-first, often anonymous social context. It was not clear to users how they should act because the product did not match the context.

In 2024, the edges and nodes of social graphs will be sliced and categorized into more specific and relevant contexts. Currently, in-protocol solutions exist (such as channels on Farcaster), but I expect out-of-protocol solutions to emerge as developers begin to demand data more relevant to the products and social experiences they want to build. I’m excited for the next wave of data primitives and developer infrastructure that will enable a new generation of social applications.

Tushar Jain

New Forms of Token Distribution

Every bull market in crypto has been kicked off by a new method of token distribution. Examples include:

- PoW chain proliferation—2013/2014

- ICOs—2017

- IEOs—2019

- Liquidity mining—2020

- NFT minting—2021

There are two new token distribution mechanisms that have developed in the recent bear market that could serve as the fuel to ignite a new bull market:

- DePIN — reward people with tokens for helping build a productive, capital asset (e.g. Helium, Hivemapper, Render).

- Points — incentivize people to use a product before all the token mechanics are worked out. Launching a token is a lot of work, and it’s much harder to change economics once the token is live. Points have no units, no max supply, and less regulatory risk because they are not transferable. Points offer an incentive in a pre-PMF sandbox.

New forms of token distribution are a powerful way to bring new users into the crypto ecosystem. I think the next big surge of users is going to come from users getting crypto assets that they earned, not bought. DePIN and Points both offer novel ways to give crypto assets to new users who have never had a crypto wallet before.

Kyle Samani

UI-Layer Composability and Client-Side ZK

UI-Layer Composability

In my 2021 presentation at the Multicoin Summit, I discussed the idea of composability. At the time, I was more focused on on-chain atomic composability. However, over the last few years, I’ve come to devalue on-chain atomic composability (hence why I changed my name on X from “Composability Kyle” to “Integrated Kyle”). Recently, the composability I have become more interested in is permissionless, UI-layer composability. In 2023, we saw the first major breakthrough in UI-layer composability: Unibot. Unibot is an on-chain terminal and DEX bot on Telegram. Whereas previously people would learn about information somewhere on the internet (X, Reddit, news, Bloomberg, Telegram chats, etc), and then navigate to a separate UI to trade (e.g., Drift, Binance, Coinbase, etc.), Unibot brought trading to Telegram, where people are already hanging out, socializing, and exchanging information.

In 2024, there is a huge opportunity to bring trading activities into many contexts around the web beyond group chats in Telegram.

Building on that idea, I hope to see more UI-layer composability, not only for asset ledgers but for social products, most notably, Farcaster. The dream of Farcaster is bold: a single event-feed in which every event is signed by a person, with myriad UIs that read and write from that event feed.

We colloquially discuss X as if X provided unique product experiences for different use cases: cryptoTwitter, fintwit, sportsTwitter, politicalTwitter, etc. There is a real opportunity to build Farcaster clients that fulfill this vision from first principles. This design space is open for the taking in 2024.

Client-Side ZK

Most of the discourse about zero knowledge (zk) over the last few years has been about scaling asset ledgers using zero-knowledge rollups and zk co-processors. However, I think the most interesting design space for zk is in client-side privacy. I recently learned about two client-side zk configurations that I find quite compelling:

- Zk.me is, as the name suggests, a system for producing zk proofs about yourself, specifically in the context of KYC and AML compliance. It is hard for me to imagine DeFi growing another 10x without more stringent on-chain KYC. Under that assumption, I prefer users not to leak their data, and zk proofs will be fundamental to fulfilling that vision.

- Brave Boomerang — traditionally, ad exchanges are run on centralized servers. This is true for Google, Facebook, and every other online ad exchange. Brave is inverting the model for ad exchanges. Users run the ad-exchange locally on their device, and submit the proof that they ran the ad exchange correctly to the blockchain. This model guarantees no PII-leakage, and still offers advertisers the granularity they seek for targeting (the zk proof can ensure that the ad for a Honda was shown to a 16 year old rather than a 6 year old).

As these two examples show, the biggest opportunities for re-imaging trust on the internet and building new business models using zk reside on the client side.

/Oracles and the New Frontier for Application-Owned Orderflow Auctions

Today, we are excited to announce our investment in Pyth Network, the leading first-party oracle in crypto.

Disclosure: Unless otherwise indicated, the views expressed in this post are solely those of the author(s) in their individual capacity and are not the views of Multicoin Capital Management, LLC or its affiliates (together with its affiliates, “Multicoin”). Certain information contained herein may have been obtained from third-party sources, including from portfolio companies of funds managed by Multicoin. Multicoin believes that the information provided is reliable and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post may contain links to third-party websites (“External Websites”). The existence of any such link does not constitute an endorsement of such websites, the content of the websites, or the operators of the websites.These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Websites. The content of such External Websites is developed and provided by others and Multicoin takes no responsibility for any content therein. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice. You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by venture funds managed by Multicoin is available here: https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced due to coordination with the development team(s) or issuer(s) on the timing and nature of public disclosure. Separately, for strategic reasons, Multicoin Capital’s hedge fund does not disclose positions in publicly traded digital assets.

This blog does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest.

Past performance does not guarantee future results. There can be no guarantee that any Multicoin investment vehicle’s investment objectives will be achieved, and the investment results may vary substantially from year to year or even from month to month. As a result, an investor could lose all or a substantial amount of its investment. Investments or products referenced in this blog may not be suitable for you or any other party. Valuations provided are based upon detailed assumptions at the time they are included in the post and such assumptions may no longer be relevant after the date of the post. Our target price or valuation and any base or bull-case scenarios which are relied upon to arrive at that target price or valuation may not be achieved.

Multicoin has established, maintains and enforces written policies and procedures reasonably designed to identify and effectively manage conflicts of interest related to its investment activities. For more important disclosures, please see the Disclosures and Terms of Use available at https://multicoin.capital/disclosures and https://multicoin.capital/terms.