下载翻译 | Descargar la traducción al mandarín

Introducción

Los registros públicos y distribuidos y la computación sin permisos, resistente a la censura y de confianza mínima van a remodelar los sectores masivos de la economía global. Esta creencia nos llevó a fundar Multicoin Capital en 2017, y después de pasar dos años con emprendedores, líderes empresariales e inversores del sector, hemos desarrollado más convicción en esta tesis que nunca antes.

En los últimos años, la amplitud de los casos de uso dentro del ecosistema de las criptomonedas se ha multiplicado. Dada esta amplitud, puede ser difícil definir las macrotesis subyacentes cuando los casos de uso comprenden activos no embargables, mercados de predicción resistentes a la censura, redes inalámbricas de pares, nuevos sistemas de publicidad en línea y empresas sin jurisdicción.

El propósito de este ensayo es definir y articular las tres megatesis de inversión para las criptomonedas. Definimos las megatesis de inversión como aquellas en las que el mercado accesible se mide en billones de dólares de 2019.

Esperamos que estas tesis se desarrollen a lo largo de una década o más y que generen la gran mayoría de nuestros rendimientos. En el orden aproximado en que esperamos que se desarrollen:

Finanzas abiertas. Al hacer que las unidades de valor, como las acciones, los bonos, los bienes inmuebles, las divisas, etc., sean interoperables, programables y componibles en registros públicos, los mercados de capitales serán más accesibles y eficientes. Así como la proliferación de los mercados de capital en los últimos 100 años permitió un nivel asombroso de creación de riqueza, las finanzas abiertas harán que los mercados de capitales sean más eficientes y accesibles para todo el mundo.

Web3. La visión de Web3 consiste en empoderar a los consumidores para que controlen sus propios datos, en lugar de la situación actual, en la que los gigantes de la tecnología, las agencias de crédito, los anunciantes, los proveedores de la salud, etc., acumulan los datos de los consumidores. A medida que este paradigma cambie, los operadores tradicionales perderán su principal ventaja competitiva, sus monopolios de datos y los efectos de la red asociados, creando oportunidades masivas para la nueva creación de valor.

Dinero global y libre de impuestos. En términos simples, se puede pensar en esto como el oro digital. Sin embargo, encontramos que el concepto de “oro digital” es demasiado limitado y subestima sustancialmente la oportunidad. El dinero global y libre de impuestos es un superconjunto de oro digital en términos de amplitud y casos de uso, y representa un mercado accesible dramáticamente más grande.

Prefacio: Confianza

El tema común que subyace a estas tesis es reducir la confianza entre las partes que realizan las transacciones. La economía moderna se basa en la acumulación de capas de confianza. Confiamos en los gigantes de la tecnología, en los bancos, en las compa�ñías de seguros, en el gobierno y en muchos más cada minuto de cada día.

Confiamos en tantas instituciones que damos por sentada la cantidad de capas de confianza en la que se basa la economía. Cuando nacemos y crecemos con ciertas suposiciones de confianza, ya ni siquiera las reconocemos como suposiciones. Dada la complejidad global, detectar los abusos de la confianza es más difícil que nunca (por ejemplo, Facebook + Cambridge Analytica, los jaqueos de Marriott/Target, el jaqueo de Equifax, etc.).

Por primera vez en la historia de la humanidad, utilizando las redes abiertas unidas mediante la criptografía y la economía de libre mercado, podemos incentivar conductas humanas específicas sin crear nuevas suposiciones de confianza. Se trata de un cambio sutil pero profundo.

Esto no quiere decir que la confianza sea intrínsecamente mala. No obstante, todo riesgo se basa en la confianza. Al crear un mundo con menos suposiciones de confianza, podemos reducir el riesgo sistémico y crear economías y sociedades más sanas y productivas.

Tesis: Finanzas abiertas

La tesis de las finanzas abiertas se denomina a veces finanzas descentralizadas o DeFi. No obstante, preferimos el término “finanzas abiertas”, ya que el nivel de (des)centralization no es la base de la tesis de inversión. La descentralización es simplemente un medio de abrir las finanzas.

La confianza es la base sobre la que se construyen todos los servicios financieros.

Aunque los mercados de capitales grandes y maduros son generalmente eficientes hoy en día, todavía no están cerca de ser universalmente accesibles. Esto es cierto tanto en los mercados desarrollados como en las economías en desarrollo.

La innovación clave que permite la financiación abierta es la modulación de las primitivas financieras. Al modularizar las primitivas financieras, la pila de las finanzas abiertas convierte la confianza en un producto básico, de modo que ninguna aplicación tiene una ventaja de confianza única sobre las demás.

La modularización de las primitivas financieras es un concepto abstracto. ¿Qué significa exactamente modularizar las primitivas financieras?

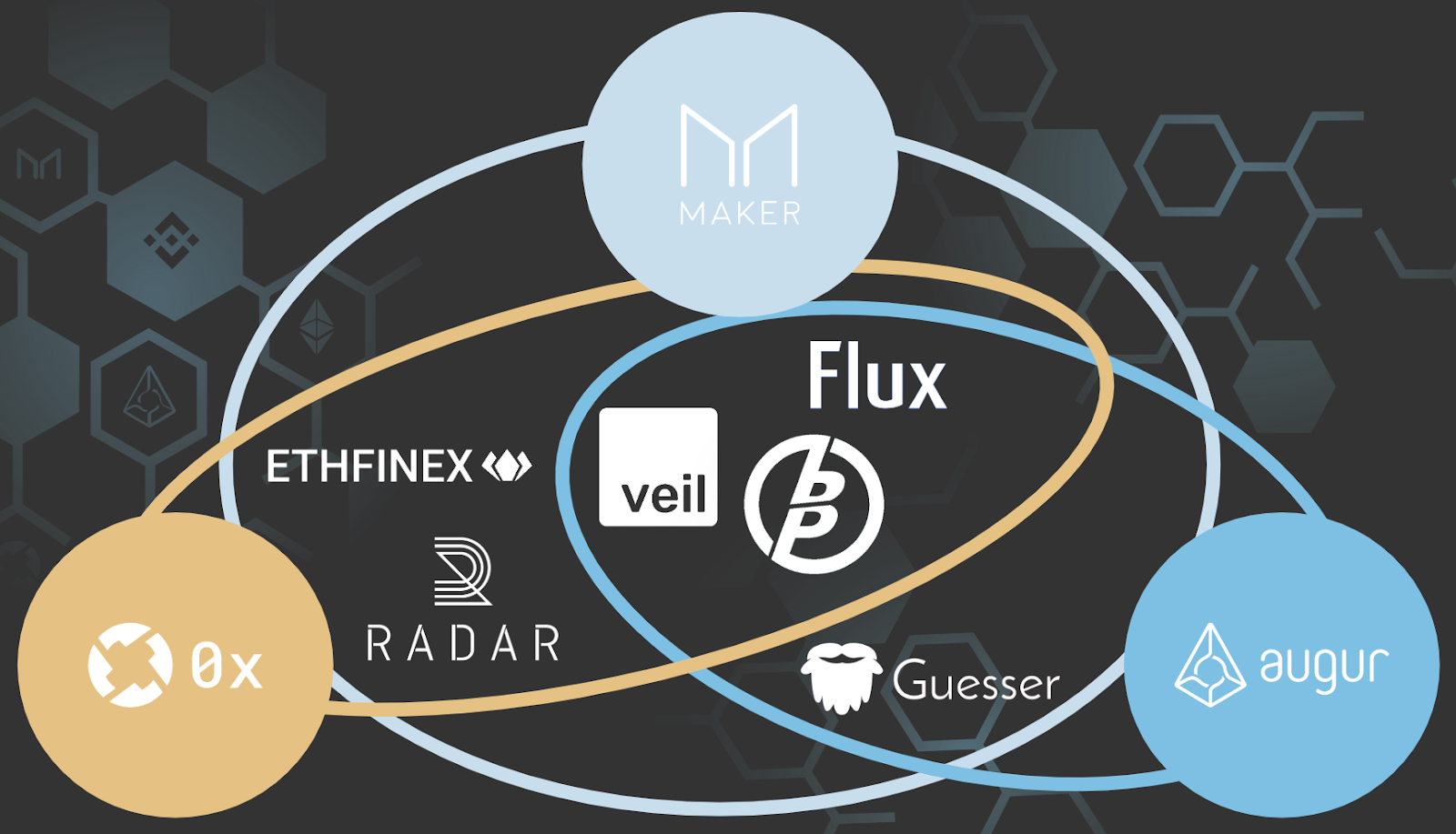

En los últimos 24 meses, se han lanzado una serie de protocolos de finanzas abiertas. Todos estos protocolos son modulares y se utilizan por aplicaciones de mayor nivel (y a menudo combinadas). Ninguno de estos protocolos comercializa con los clientes finales, ni ofrece servicio al cliente, ni se ocupa de las leyes locales. Estos protocolos son solo piezas de código que viven en cadenas de bloques. Esto es comparable a la forma en que el correo electrónico se construye sobre un conjunto de protocolos abiertos como SMTP, TCP/IP y HTML/JS para representar el correo electrónico en el navegador.

Tomemos como ejemplo BlitzPredict (BP). BP es un intercambio centrado en las apuestas deportivas que se ha creado sobre los protocolos Augur, 0x y (en un futuro cercano) Maker. BP se basa en el protocolo Augur como un medio para crear diferentes tipos de mercados, crear acciones en esos resultados y, en última instancia, resolver los mercados. BP se basa en el protocolo 0x para intercambiar acciones entre usuarios. Y BP pronto se basará en el protocolo Maker para su stablecoin colateralizada, DAI, para denominar las operaciones. Cada uno de estos protocolos funcionan de forma independiente. Debido a que son modulares, una aplicación de mayor nivel como BP puede combinar las primitivas financieras subyacentes para producir una experiencia de usuario minimizada de la confianza que nunca antes fue posible.

Del mismo modo que la nube ha convertido los despliegues de servidores en productos básicos, lo que permite una mejora de la función escalonada en la tasa de innovación en las aplicaciones web a gran escala, la modularización de las primitivas financieras permitirá una mejora de la función escalonada en la tasa de innovación en todos los servicios financieros.

Como las finanzas abiertas son... abiertas, cualquiera será capaz de crear empresas locales sobre los protocolos de finanzas abiertas. Así es como las finanzas abiertas permitirán el acceso a los servicios financieros a las personas que no lo tienen o que tienen un acceso restringido. Los protocolos no servirán a los consumidores. Las empresas que navegan por las regulaciones locales y proporcionan un servicio al cliente localizado servirán a los consumidores en su lugar.

Un gran ejemplo de esto es el protocolo UMA. El protocolo UMA es una plataforma que permite a dos partes celebrar un contrato por diferencia (CFD) que se reequilibra constante y automáticamente a medida que el precio del activo subyacente se mueve en tiempo real. El primer producto creado con el protocolo UMA fue la exposición sintética al S&P 500. El equipo de UMA tiene su sede en los EE. UU., y no es un corredor de bolsa registrado. El equipo de UMA no comercia con el protocolo que creó.

Por el contrario, los creadores de mercado de todo el mundo están proporcionando liquidez y cubriendo su riesgo en los mercados de capitales tradicionales, lo que permite a cualquier persona del mundo obtener exposición al S&P 500 sin pagar ninguna comisión (UMA no cobra ninguna comisión), sin pasar por ningún intermediario y sin asumir ningún riesgo de contrapartida (el contrato inteligente de UMA actúa como un agente depositario minimizado de la garantía que cada parte deposita). A medida que los 4 a 5 mil millones de personas que no tienen acceso o tienen acceso restringido a los servicios bancarios en todo el mundo acceden al dinero digital, es natural que quieran invertir en activos a los que no tienen acceso. Las normas que rigen los mercados de valores de EE. UU. dificultan que este subconjunto de personas obtenga el acceso que desean. Ahora bien, con protocolos como el UMA, la inclusión financiera global será posible por primera vez en la historia de la humanidad.

No podemos exagerar la magnitud de este avance. Por primera vez, los mercados financieros pueden ser globales, sin permisos y, para muchos tipos de contratos de derivados, libres de riesgo de contraparte. Esto era imposible hasta hace poco.

La infraestructura de los mercados financieros del mundo se trasladará a la pila de las finanzas abiertas porque esta permite que millones de empresas, de escala local, nacional e internacional, ofrezcan productos financieros de confianza minimizada a las personas y empresas que más los necesitan. A diferencia de las instituciones financieras heredadas, la próxima generación de empresas de criptomonedas nativas no necesitará ser de confianza, ni tendrá que construir ninguna tecnología nueva o particularmente novedosa. La pila de finanzas abiertas convertirá en productos básicos las primitivas financieras sobre las que se realizan todas las transacciones, permitiendo un flujo de capital realmente fluido entre clases de activos y jurisdicciones. A medida que estas empresas de criptomonedas nativas prosperan, los operadores tradicionales se verán obligados a cambiar también a la pila de finanzas abiertas.

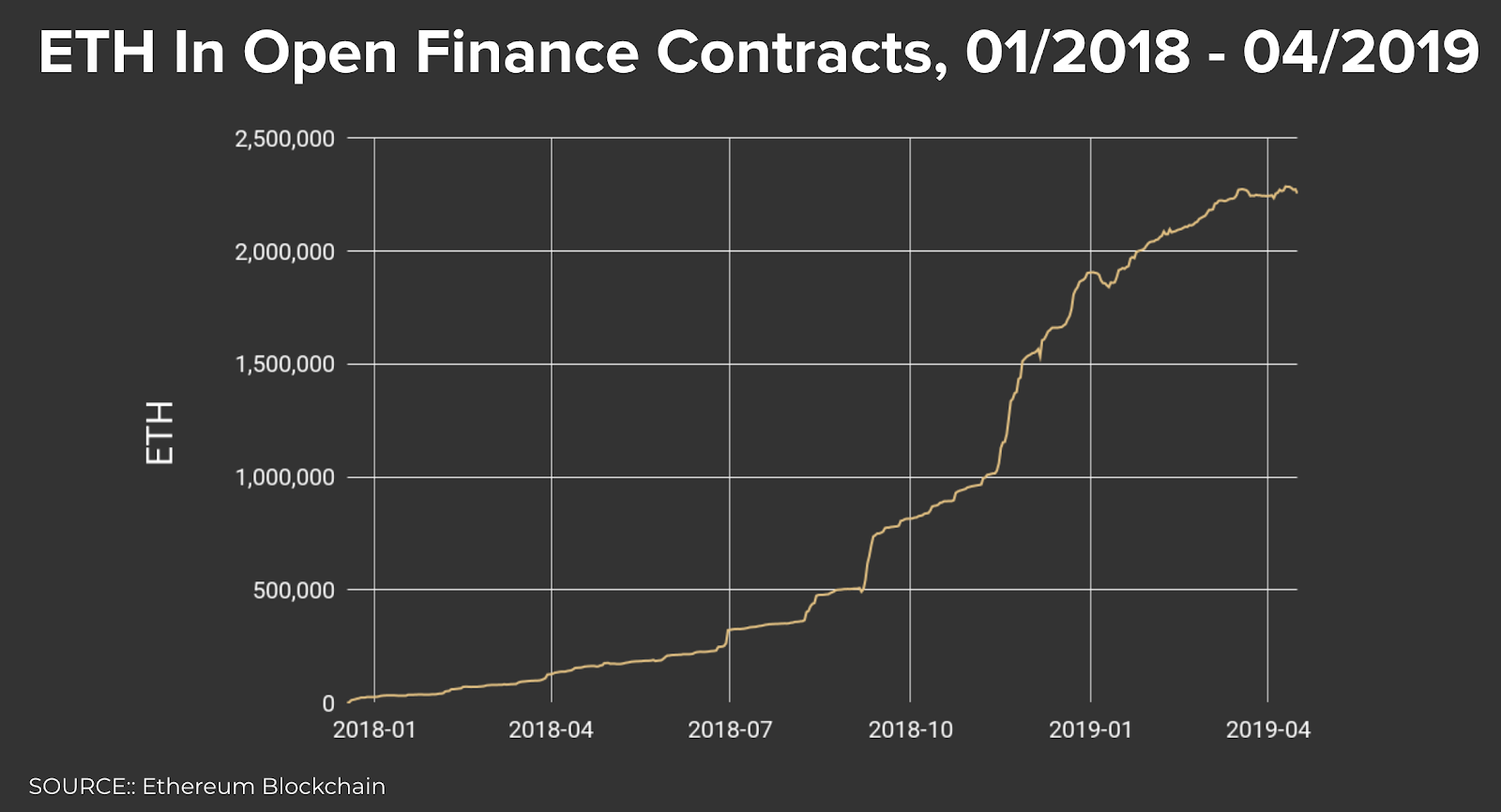

Las finanzas abiertas no son teóricas. Está sucediendo ahora, y esperamos que esta megatendencia se agrave en la próxima década. En los últimos 18 meses, la cantidad de capital bloqueado en los contratos inteligentes de finanzas abiertas ha aumentado de 0 dólares a más de 400 millones de dólares.

Hemos estado evaluando e invirtiendo en protocolos de finanzas abiertas y compañías desde el inicio del fondo en 2017. Los ejemplos incluyen protocolos como Augur, Maker y 0x, y las compañías que se basan en estos protocolos como Dharma, BlitzPredict y Radar Relay (nota: estos son ejemplos ilustrativos. Multicoin Capital no se invierte necesariamente en todos ellos).

Tesis: Web3

Al igual que las finanzas abiertas se basan en la modularización de las primitivas financieras, Web3 se basa en la desagregación de la propiedad de los datos y la lógica de las aplicaciones. Históricamente, las aplicaciones de Web2 combinaron el almacenamiento de datos y la lógica de aplicaciones. El cambio paradigmático en Web3 es la desagregación de los datos y la lógica de las aplicaciones. Al desagregar lo que se incluyó anteriormente, los propietarios de los datos no necesitarán confiar en los proveedores de las aplicaciones con sus datos.

Chris Dixon de la criptomoneda de a16z expuso la tesis de Web3 en Por qué es importante la descentralización. Dixon sostiene que las plataformas centralizadas como Google y Facebook, debido a sus obligaciones fiduciarias con los accionistas, pasan intrínsecamente de proporcionar valor a extraerlo de sus respectivos ecosistemas, como se muestra a continuación:

Basándonos en el ensayo de Dixon, definiremos Web3 más específicamente como la propiedad y el control autosoberano de los datos. Esto es un corolario a la caracterización de Dixon sobre la descentralización de las redes: si las redes se descentralizan, no habrá un servidor central que sea propietario y controle los datos de los usuarios; en su lugar, los usuarios serán propietarios y controlarán sus propios datos.

Las diferencias arquitectónicas de alto nivel entre Web2 y Web3 son claras: en el modelo Web2, las compañías controlan las bases de datos cerradas y son propietarias de los datos de los usuarios, tanto técnica como legalmente. En el modelo Web3, los usuarios son propietarios de sus propios datos encriptados en redes abiertas arquitectónicamente como el Sistema de Archivos Interplanetarios (IPFS, por sus siglas en inglés), e interactúan entre sí utilizando mensajes firmados criptográficamente en plataformas de contratos inteligentes que actúan como registros públicos y programables.

Hoy los monopolios de Internet utilizan los datos de los consumidores en contra del mejor interés de sus usuarios (por ejemplo, el intercambio y la venta no autorizados de los datos de los usuarios o la vigilancia generalizada de la web). Además, los monopolios de los datos evitan la innovación al limitar los tipos de aplicaciones que se pueden crear sobre estos valiosos conjuntos de datos.

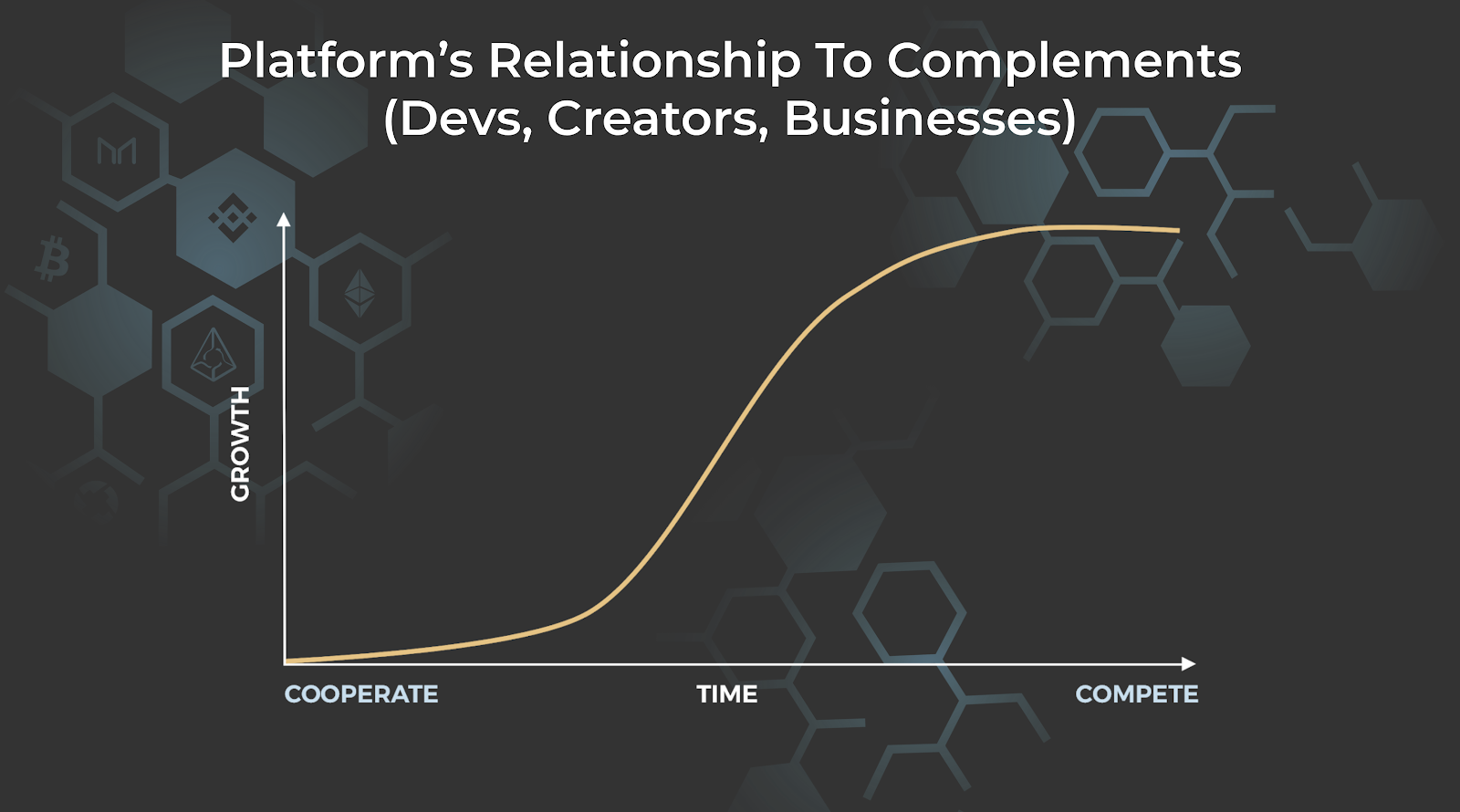

Cuando los usuarios sean propietarios de sus propios datos, los monopolios de datos se desmoronarán. Los efectos de segundo y tercer orden de esto crearán nuevas y masivas oportunidades. De la misma manera que nadie pudo prever con precisión la tasa de innovación del software construido sobre los sistemas operativos en la década de 1980, o la aparición de aplicaciones web compuestas por docenas de servicios en la nube en 2009, la desintegración de los silos de los datos potenciará la mayor coopetición de los desarrolladores (cuando los competidores cooperan) que el mundo haya visto jamás. Hace aproximadamente un año, describimos cómo podría ser la coopetición de los desarrolladores (aunque de una manera bastante rudimentaria) en el contexto de las aplicaciones de las redes sociales.

Es difícil imaginar cómo un conjunto de compañías construidas sobre la pila Web3 desplazará a los operadores tradicionales con los monopolios de datos construidos sobre la pila Web2. Quizás el argumento más destacado contra Web3 sea “Los consumidores no se preocupan por la privacidad o la propiedad de los datos”.

Estamos de acuerdo. Los consumidores no cambiarán a alternativas basadas en Web3 por razones ideológicas. Cambiarán por razones utilitarias.

A medida que la pila Web3 vaya madurando, los desarrolladores y los emprendedores elegirán explícitamente crear aplicaciones en la pila Web3 en lugar de en la pila Web2. ¿Por qué? Porque los emprendedores han aprendido a no confiar en los monopolios Web2. Como señaló Dixon en “Por qué es importante la descentralización”: “Con el tiempo, los mejores emprendedores, desarrolladores e inversionistas se han vuelto cautelosos a la hora de crear sobre las plataformas centralizadas. Ahora tenemos décadas de evidencia de que hacerlo terminará en decepción”.

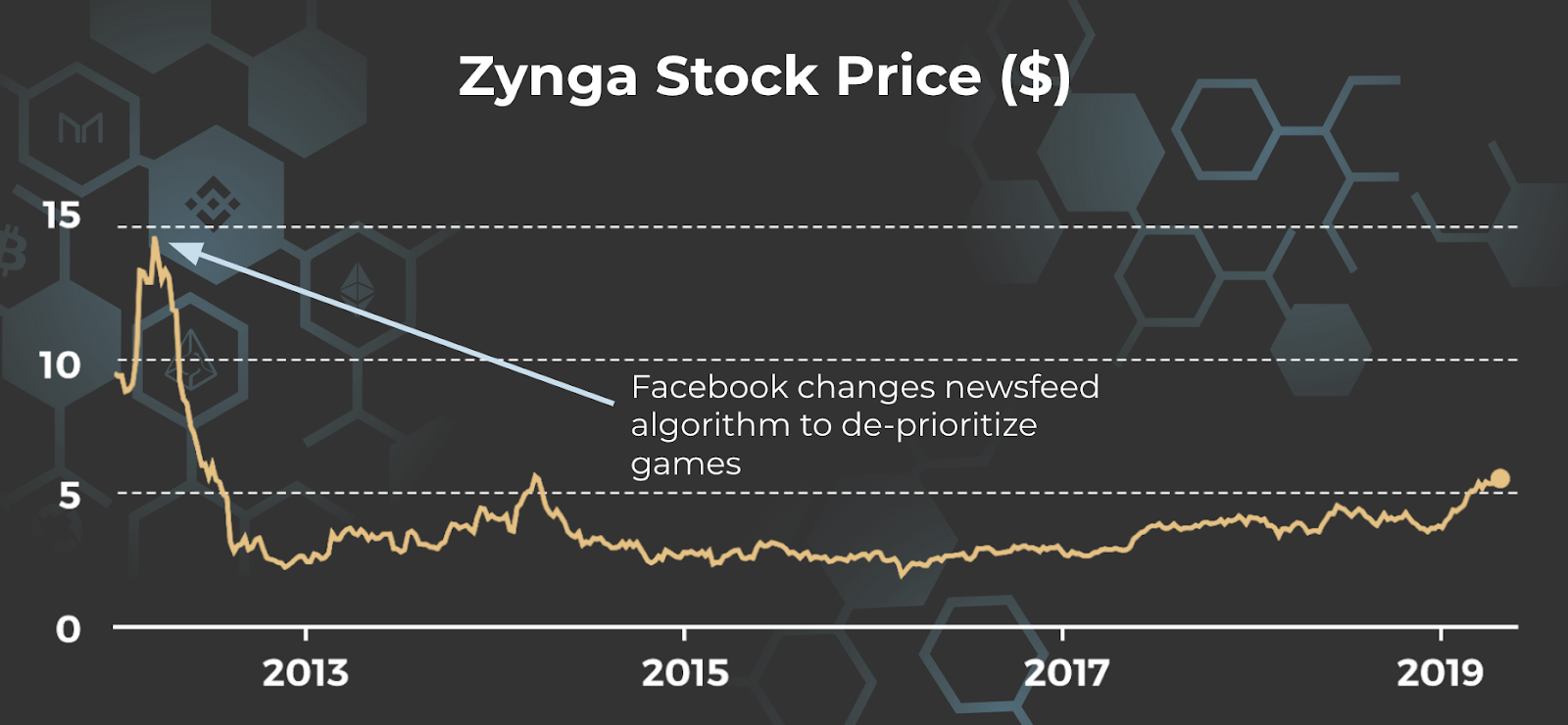

Miles de compañías, desde Yelp hasta Zynga o Buzzfeed, se han dado cuenta de que los monopolios Web2 no son proveedores de plataformas confiables. Por lo tanto, los desarrolladores y los emprendedores se basarán en la pila Web3 y buscarán maneras de ofrecer mejores productos y servicios a los consumidores.

Consideremos el protocolo Tari. El protocolo Tari está muy centrado en la emisión de activos digitales y está comenzando a centrarse en los boletos para los conciertos y otros eventos en directo. El equipo de Tari se dio cuenta de que había una oportunidad de replantear la emisión de los activos digitales y la venta de los boletos para resolver los dos problemas más grandes de la industria: el fraude de los boletos y los revendedores.

Naveen Jain, Dan Teree y Riccardo Spagni fundaron Tari. Naveen dirigió anteriormente la tecnología de artistas como Linkin Park, Bon Jovi, Lil Wayne y Carrie Underwood; Dan fundó anteriormente Ticketfly, que Pandora adquirió por 450 millones de dólares; y Riccardo es el principal encargado de mantener Monero, que es una de las criptomonedas más antiguas y valiosas.

Los emprendedores de este calibre saben que los monopolios Web2 como TicketMaster no son de fiar. Nunca crearán sobre TicketMaster. En cambio, eligen crear sobre la pila Web3.

La visión de Web3 tiene un alcance extremadamente ambicioso. Hasta el nacimiento de Ethereum, nadie estaba construyendo un software que soportara los datos autosoberanos de los usuarios. Crear una pila tecnológica de confianza mínima que rivalice el rendimiento y la escala de Web2 es una tarea enorme. Hoy en día, hay cientos de equipos en todo el mundo que construyen la pila Web3 para soportar la computación de confianza mínima sobre los datos autosoberanos.

La pila Web3 es todavía joven. Con todo, ya podemos ver los primeros atisbos de su funcionamiento, y estamos invirtiendo en protocolos y compañías que se centran en aplicaciones específicas, como Tari, y en las que construyen la infraestructura básica de esta nueva pila tecnológica. Hemos invertido en The Graph, Keep, Livepeer, SKALE, Spring Labs, StarkWare y Textile, cada uno de los que proporciona una infraestructura crítica en la pila Web3.

Tesis: Dinero global libre de impuestos

Como el dinero fiduciario está obligado por la confianza en las instituciones humanas y no por la física, tenemos que depositar una inmensa confianza en las instituciones humanas que gobiernan el dinero.

Existe una enorme oportunidad para un dinero de confianza mínima. Un activo al portador, nativamente digital, que se rija por la física, las matemáticas y la economía de libre mercado en lugar de por las instituciones humanas. Ese dinero será la medida global y libre de impuestos del valor, es decir, el dinero.

La forma más sencilla de pensar en la oportunidad de un dinero global y libre de impuestos es el oro digital. Aunque este planteamiento no es erróneo, subestima enormemente la oportunidad.

Es claro cómo los tokens de la capa 1 de la cadena de bloques como el Bitcoin son superiores al oro: los activos digitales son infinitamente divisibles y transportables a nivel global, y sus horarios de suministro son 100 % auditables y transparentes. Debido a estos atributos, la oportunidad de un dinero libre de impuestos supera con creces la del oro. Hemos sostenido que el mercado al que puede acceder este dinero libre de impuestos es de 100 billones de dólares, mientras que el del oro es de entre 7 y 8 billones de dólares. Una recapitulación de los argumentos que hemos expuesto anteriormente:

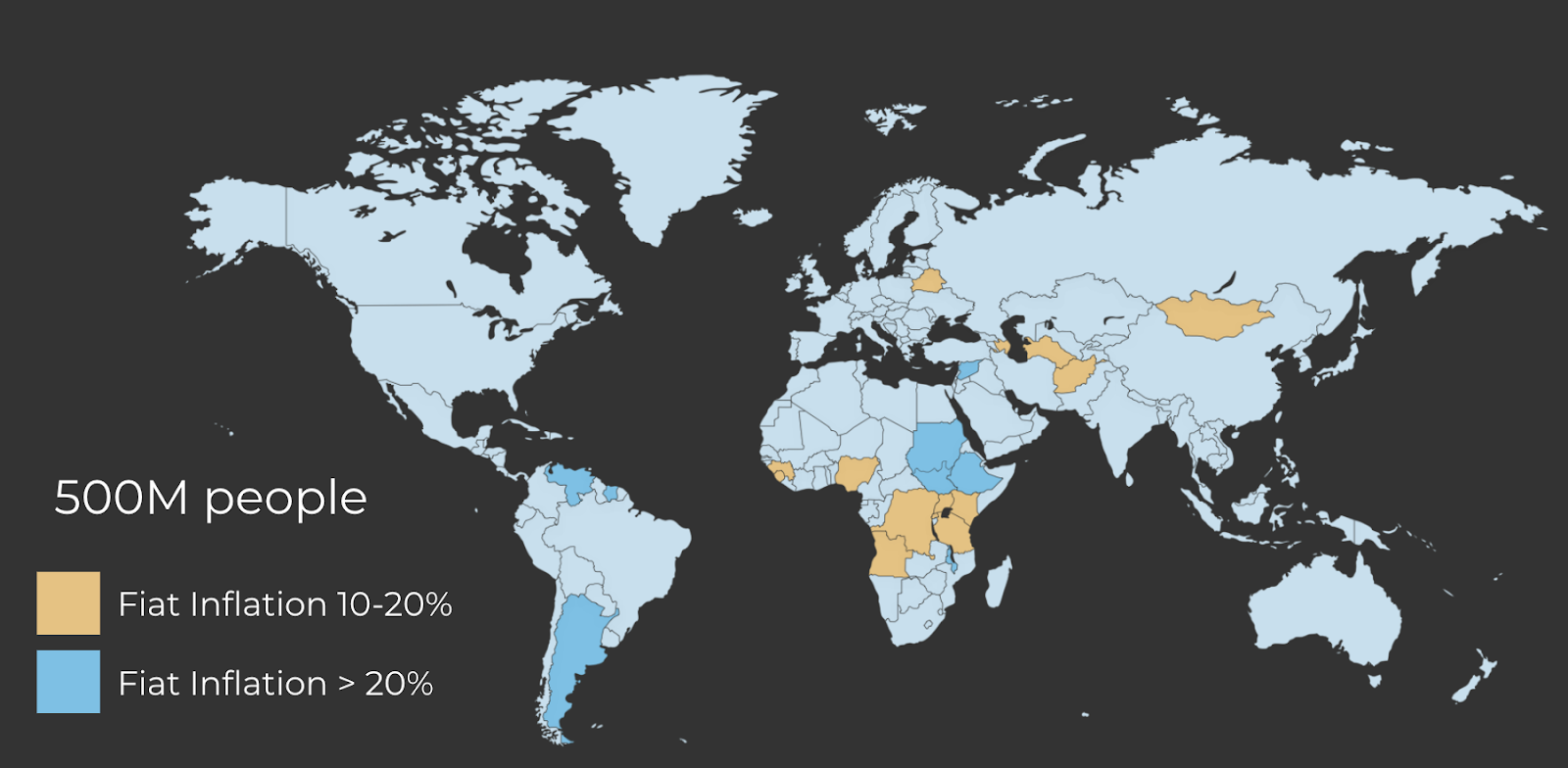

1) El dinero libre de impuestos expande el mercado del oro de la misma manera que Uber amplió el mercado de los taxis. Precisamente las personas que más necesitan dinero resistente a la inflación, los 500 millones de personas que viven en países con una inflación anual superior al 10 %, no pueden almacenar físicamente su riqueza en oro y, en general, no tienen acceso a los mercados de capitales para que puedan adquirir derechos sobre el oro en una bóveda.

2) Contrariamente a la intuición, las personas más ricas quieren activos resistentes a la incautación incluso más que las personas que viven en países con hiperinflación. Su máxima prioridad es no perder su riqueza, y las criptomonedas actúan como una “cuenta bancaria suiza en el bolsillo”. Se estima que hay entre 20 y $30 billones de dólares escondidos en las cuentas bancarias en el extranjero en todo el mundo.

3) A diferencia del oro, que no ofrece un rendimiento orgánico, los fondos basados en la cadena de bloques garantizan tasas perpetuas, positivas y libres de riesgos (a través de la participación en las redes de prueba de participación, y a través del enrutamiento de la liquidez en las redes de canales de pago sobre las redes de prueba de trabajo). Muchos inversionistas, como Warren Buffet, se niegan a invertir en metales preciosos porque no generan rendimientos. Del mismo modo, muchos inversionistas y fondos institucionales grandes solo invierten en acciones que pagan un dividendo, excluyendo a compañías como Amazon. Debido a que los fondos digitales ofrecen tasas nativas libres de riesgo, una enorme cantidad de nuevo capital neto invertirá en fondos digitales que no puede invertir en oro hoy en día.

4) Actividad económica nueva: los ecosistemas de finanzas abiertas y Web3 desbloquearán billones de dólares de actividad económica en las cadenas de bloques. Deberíamos esperar que al menos parte de esto fluya hacia los tokens nativos que alimentan estas cadenas de bloques.

Una vez comprendida la oportunidad de un dinero libre de impuestos, la pregunta obvia es: ¿qué dinero o fondos serán? Dados los efectos de la red del dinero, creemos que habrá una convergencia natural a largo plazo hacia un único dinero libre de impuestos.

Y ese dinero es poco probable que sea Bitcoin.

Hay tres hipótesis principales que describen la ruta por la que un activo puede convertirse en el dinero global y libre de impuestos.

La primera es la hipótesis SOV, que sostiene que la única propiedad del dinero que importa (más allá de la seguridad básica y la usabilidad) es su política monetaria y, por lo tanto, que el dinero menos inflacionario debe ganar. Este punto de vista es el que más defienden los maximalistas del Bitcoin.

La segunda es la hipótesis de utilidad que sostiene que el dinero que se utiliza como dinero se convertirá en el dinero global y libre de impuestos. Los defensores de esta hipótesis también reconocen la necesidad de una política monetaria previsible y creíble. Sin embargo, no necesariamente la priorizan como la única variable que dictará qué token de la cadena de bloques nativa se convertirá en el dinero global y libre de impuestos. Este punto de vista es el que más defienden las personas que construyen en y sobre plataformas de contratos inteligentes, ya que estas plataformas son las que tienen más probabilidades de producir la mayor utilidad al impulsar los ecosistemas de finanzas abiertas y Web3.

La tercera es la hipótesis de la stablecoin, que sostiene que la estabilidad de los precios es necesaria para que se adopte una moneda. No obstante, las stablecoins están sujetas a compensaciones intrínsecas, y nos parece extremadamente improbable que cualquier stablecoin algorítmica sobreviva a la prueba del tiempo debido a la trinidad de la imposibilidad.

Creemos que la hipótesis de la utilidad es la que tiene más probabilidades de producir el dinero más valioso, es decir, que el dinero que la gente utiliza como dinero en una gran variedad de aplicaciones se convertirá en el dinero global y libre de impuestos, y como tal, invertimos una gran parte de nuestro tiempo y energía en plataformas de contratos inteligentes y en la infraestructura necesaria para ayudarles a cumplir las visiones de las finanzas abiertas y de la Web3. Aunque Ethereum es actualmente el líder del mercado en este ámbito, no lo damos por sentado que vaya a ganar, sino que gestionamos nuestra cartera de forma probabilística.

Conclusión

La economía es una máquina maravillosamente compleja. Que funcione a una escala tan increíble es un testimonio del poder de la confianza que subyace en nuestras instituciones humanas.

Aunque la economía y la sociedad se basan en una inmensa cantidad de confianza, esta no es perfecta. Los seres humanos fallan. Y, por lo tanto, las instituciones humanas fallan. Los fallos pueden agravarse, creando fallos en cascada y riesgo sistémico.

Gracias a las redes abiertas que se basan en las suposiciones de libre mercado y limitadas por la criptografía, los seres humanos pueden, por primera vez en la historia, coordinar a gran escala sin introducir intermediarios de confianza que puedan abusar de ella. Ahora que esto es posible, podemos revisar todas nuestras suposiciones de confianza preconcebidas en muchos sectores de la economía y crear cantidades increíbles de valor económico.

La transición de una economía de confianza a una de autosoberanía estará detrás de una de las mayores transferencias de riqueza de la historia humana.

La confianza es la base de todas las relaciones económicas. La mayor oportunidad de inversión de nuestra vida es apostar que no tiene por qué serlo.

La tesis de inversión de Multicoin Capital, las “Megatesis de las criptomonedas”, se presentó por primera vez en la cumbre de Multicoin celebrada en la primavera de 2019. Mira la presentación completa a continuación.

*Información: Multicoin Capital mantiene posiciones en algunos de los activos comentados en este artículo. Multicoin Capital se rige por una «política de no negociación» para los activos enumerados en este informe durante los 3 días («período de no negociación») siguientes a su publicación. Ningún funcionario, directivo ni empleado comprará ni venderá ninguno de los activos antes mencionados durante el Período de no negociación.*

En la fecha de publicación de este informe, Multicoin Capital Management LLC y sus filiales (colectivamente “Multicoin”), otros que contribuyeron en la investigación para este informe y otros con los que hemos compartido nuestra investigación (colectivamente, los “inversionistas”) son propietarios de tokens del proyecto aquí descrito, y pueden materializar ganancias en caso de que el precio del token aumente o disminuya. Tras la publicación del informe, los inversionistas podrán operar con los tokens del proyecto aquí descrito. Todo el contenido de este informe representa las opiniones de Multicoin. Multicoin obtuvo toda la información aquí considerada de fuentes que cree son exactas y confiables. Sin embargo, dicha información se presenta “tal como está”, sin garantía de ningún tipo, ya sea expresa o implícita.

Este documento es solo para fines informativos y no tiene la intención de ser una confirmación oficial de ninguna transacción. Los precios, datos y otra información de mercado no están garantizados en cuanto a la integridad o exactitud, se basan en datos seleccionados del mercado público y reflejan las condiciones prevalentes y las opiniones de Multicoin a esta fecha, todo lo cual está sujeto a cambios sin previo aviso. Multicoin no está en la obligación de continuar proporcionando informes sobre el proyecto. Los informes se preparan según la fecha indicada y pueden volverse poco fiables como resultado de circunstancias posteriores del mercado o económicas.

Cualquier inversión implica riesgos sustanciales, incluidos, entre otros, la volatilidad de los precios, una liquidez inadecuada y la posible pérdida completa de capital. El valor fundamental estimado de este informe solo representa la mejor estimación de la valoración fundamental potencial de un token específico y, ni de manera expresa ni implícita, es una valoración de la calidad de un token, un resumen de rendimientos pasados o una estrategia de inversión factible para un inversionista.

Este documento no constituye en modo alguno una oferta o una solicitud de oferta de compra o venta de alguna inversión o token aquí discutido.

La información contenida en este documento puede incluir o incorporar, por referencia, declaraciones prospectivas, las cuales comprenderán cualquier declaración que no sea la declaración de un hecho histórico. Estas declaraciones prospectivas pueden resultar incorrectas y pueden verse afectadas por supuestos inexactos o por riesgos, incertidumbres y otros factores conocidos o desconocidos, la mayoría de los cuales está fuera del control de Multicoin. Los inversionistas deben llevar a cabo una diligencia debida independiente con la asistencia de profesionales expertos en finanzas, derecho y tributación para todos los tokens discutidos en este documento y desarrollar un criterio independiente acerca de los mercados relevantes antes de tomar cualquier decisión de inversión.

/On Value Capture at Layers 1 and 2

Among the crypto development and investor communities, the most popular term is “protocol,” and for good reason. Everyone is building a protocol (and presumably these protocols offer investors and employees some way to generate returns).

Disclosure: Unless otherwise indicated, the views expressed in this post are solely those of the author(s) in their individual capacity and are not the views of Multicoin Capital Management, LLC or its affiliates (together with its affiliates, “Multicoin”). Certain information contained herein may have been obtained from third-party sources, including from portfolio companies of funds managed by Multicoin. Multicoin believes that the information provided is reliable and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post may contain links to third-party websites (“External Websites”). The existence of any such link does not constitute an endorsement of such websites, the content of the websites, or the operators of the websites.These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Websites. The content of such External Websites is developed and provided by others and Multicoin takes no responsibility for any content therein. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice. You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by venture funds managed by Multicoin is available here: https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced due to coordination with the development team(s) or issuer(s) on the timing and nature of public disclosure. Separately, for strategic reasons, Multicoin Capital’s hedge fund does not disclose positions in publicly traded digital assets.

This blog does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest.

Past performance does not guarantee future results. There can be no guarantee that any Multicoin investment vehicle’s investment objectives will be achieved, and the investment results may vary substantially from year to year or even from month to month. As a result, an investor could lose all or a substantial amount of its investment. Investments or products referenced in this blog may not be suitable for you or any other party. Valuations provided are based upon detailed assumptions at the time they are included in the post and such assumptions may no longer be relevant after the date of the post. Our target price or valuation and any base or bull-case scenarios which are relied upon to arrive at that target price or valuation may not be achieved.

Multicoin has established, maintains and enforces written policies and procedures reasonably designed to identify and effectively manage conflicts of interest related to its investment activities. For more important disclosures, please see the Disclosures and Terms of Use available at https://multicoin.capital/disclosures and https://multicoin.capital/terms.