Ethena: Synthetic Dollars Challenge Stablecoin Duopoly

Today, we’re proud to announce that our liquid fund invested in ENA, the native token for Ethena Protocol, the issuer of USDe, the leading synthetic dollar.

In our blogpost, The Endgame for Stablecoins, we stated how stablecoins are the largest addressable markets in crypto and how yield is the final frontier. While we were directionally right on yield-bearing stablecoins, we underestimated the market size for synthetic dollars.

We divide stablecoin as a category into two parts:

- Ones that share yield, and

- Ones that don’t

Stablecoins that share yield can be further divided into two parts

- Ones that are always entirely backed 1:1 by government-backed treasury assets

- Ones that aren’t: Synthetic dollars

Synthetic Dollars are not entirely backed by government backed treasury assets; instead, they aim to generate yield and create stability by executing delta-neutral trading strategies in financial markets.

Ethena is a decentralized protocol, an operator of the largest synthetic dollar USDe.

Ethena aims to provide a stable alternative to traditional stablecoins like USDC and USDT whose reserves earn roughly short-term U.S. treasury yields. Ethena’s USDe reserves generate yield and target stability through one of the largest and proven strategies in traditional finance: the basis trade.

The basis trade on US treasury futures alone is measured in hundreds of billions, if not trillions, of dollars. Today, access to hedge funds that have the infrastructure to do basis trades at scale is reserved for accredited investors and qualified institutional purchasers. Crypto is rebuilding the financial system from the ground up, making such opportunities accessible to everyone through tokenization.

As a team, we’ve been thinking about a synthetic dollar built on the basis trade for years. Back in 2021, we published an essay outlining this opportunity and announced our investment in UXD Protocol — the first token fully backed by a basis trade.

While UXD Protocol was ahead of its time, Guy Young — founder and CEO of Ethena Labs — has, in our opinion, executed this vision exceptionally well. Today, Ethena stands as the largest synthetic dollar, growing to $15B in circulation within two years of launch before correcting to ~$8B after the October 10 market washout. It is the third-largest digital dollar overall, after USDC and USDT.

Source: DefiLlama

Source: DefiLlama

The Systemic Tailwinds for Synthetic Dollars

Ethena sits at the intersection of three powerful trends reshaping modern finance: stablecoins, perpification, and tokenization.

Stablecoins

There are over $300 billion in stablecoins currently in circulation, and that number is expected to grow into the trillions by the end of the decade. For nearly a decade, USDT and USDC have dominated the stablecoin market, together accounting for more than 80% of total supply. Neither shares yield directly with holders — but we believe that, over time, yield-sharing with users will become the norm rather than the exception.

In our view, stablecoins compete and differentiate across three key vectors: distribution, liquidity and yield.

Tether has built exceptional liquidity and global distribution for USDT. It serves as the primary quote asset in crypto trading and is the most widely used way to access digital dollars in the emerging market.

Circle has focused on acquiring distribution by sharing economics with partners like Coinbase — a strategy that, while effective for growth, puts pressure on Circle’s margins. As crypto adoption accelerates, we expect more companies with deep distribution across finance and technology to issue their own stablecoins, further commoditizing the treasury-backed stablecoin market.

For new entrants in the digital dollar space, the main way to stand out has been through higher yields. Over the past few years, the narrative around yield-bearing stablecoins has gained momentum. However, those backed by U.S. Treasuries haven’t offered enough yield to drive meaningful adoption within crypto. The reason is because the opportunity cost of capital for crypto natives has historically been higher than US Treasury yields.

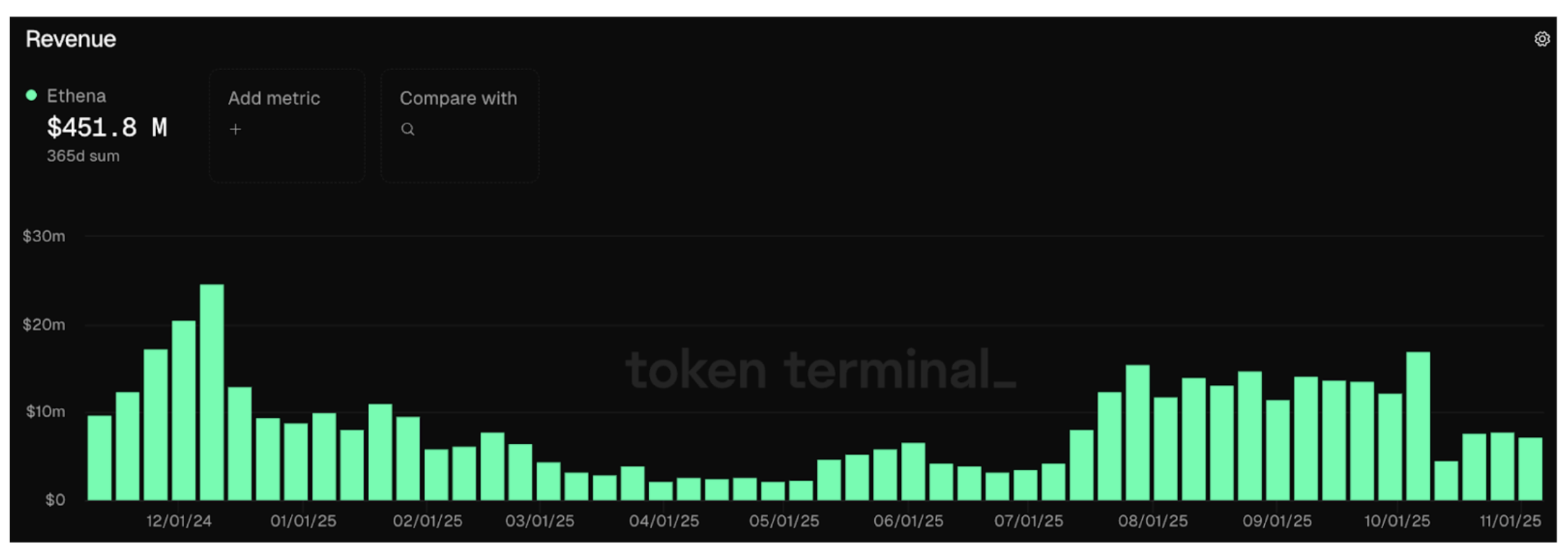

Among the new entrants, Ethena is the only one to achieve meaningful distribution and liquidity, largely because it offered higher yields. Based on sUSDe’s price change since inception, we estimate its annualized yield since inception at slightly over 10%, more than twice that of treasury-backed stablecoins. It does so by harnessing the basis trade, a strategy that monetizes the market’s demand for leverage. Since inception, the protocol has generated close to $600 million in revenue — with over $450 million of that produced in just the past twelve months.

Source: Token Terminal

Source: Token Terminal

In our view, the true test of a synthetic dollar’s adoption is its acceptance as collateral on major exchanges. Ethena has done an exceptional job integrating USDe as a core form of collateral on major centralized exchanges like Binance and Bybit, a key driver of its rapid growth.

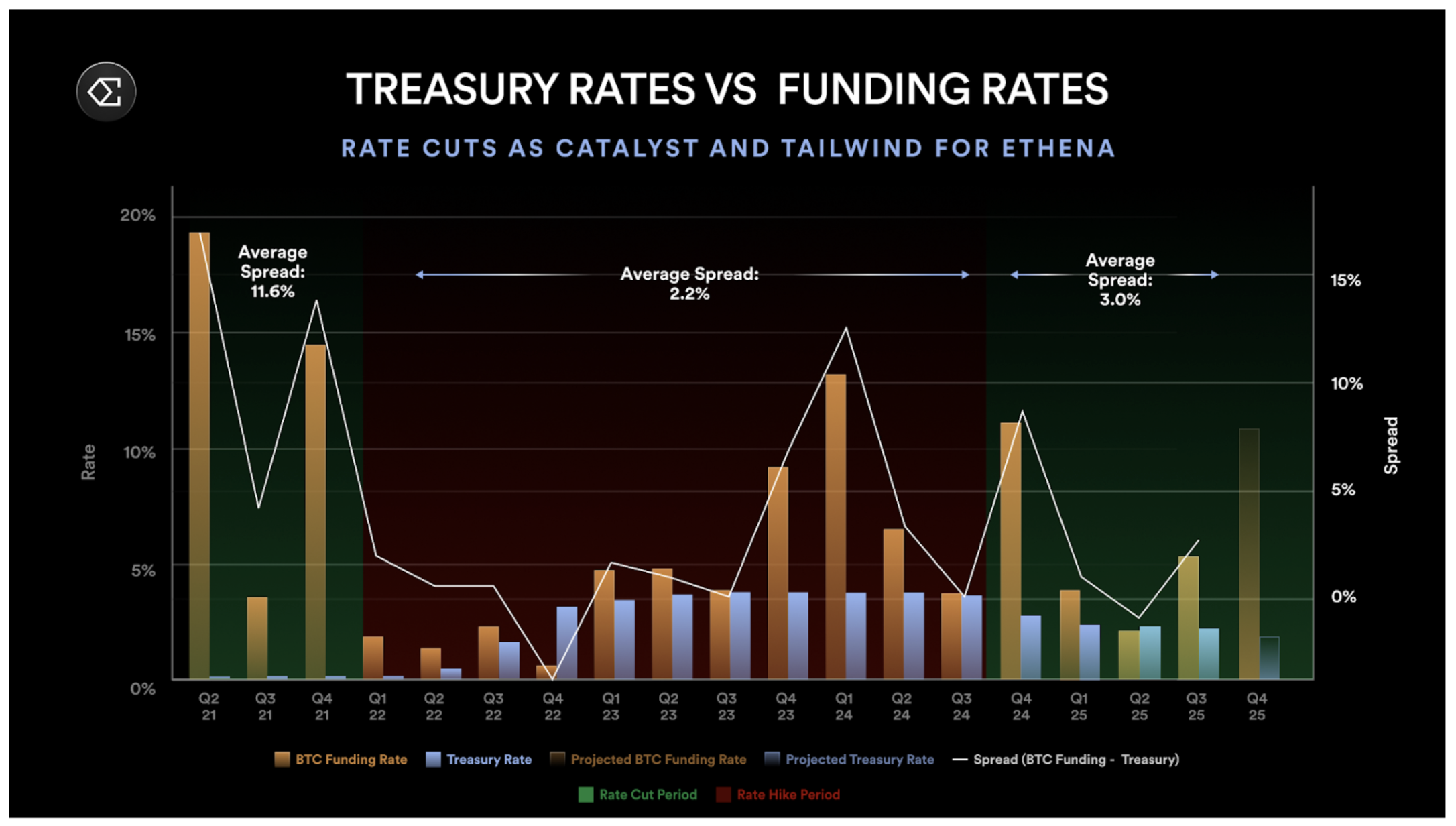

Another unique aspect of Ethena’s strategy is its mild negative correlation with Fed Funds rates. Unlike Treasury-backed stablecoins, Ethena is expected to benefit when rates fall — because lower rates stimulate economic activity, increase demand for leverage, lead to higher funding rates and strengthen the basis trade that underpins Ethena’s yield. We have seen a version of this playout in 2021 when the spread between funding rates and treasury rates widened beyond 10%.

While it is true that as crypto integrates with traditional financial markets, more capital will flow into the same basis trade and narrow the spread between the basis trade and Fed Funds rates, this integration will take years.

Sources: BTC funding rates, Treasury rates

Sources: BTC funding rates, Treasury rates

Lastly, J.P. Morgan projects that yield-bearing stablecoins could capture up to 50% of the stablecoin market in the coming years. With the total stablecoin market expected to soar into trillions, we believe Ethena is well-positioned to be a major player in that shift.

Perpification

Perpetual futures have achieved strong product–market fit in crypto. In a roughly $4 trillion asset class that is crypto, perpetual contracts trade more than $100 billion per day with an open interest of more than $100B across CEX and DEX. They offer an elegant way for investors to gain leveraged exposure to the price movements of an underlying asset. We believe that more asset classes over time will adopt perpetuals, and that is what we mean by perpification.

A common question about Ethena is the size of its addressable market, as its strategy’s scale is constrained by the open interest in perpetuals markets. We agree this is a fair constraint in the short term — but believe it underestimates the opportunity over the medium- to long-term.

Perpetuals on Tokenized Equities

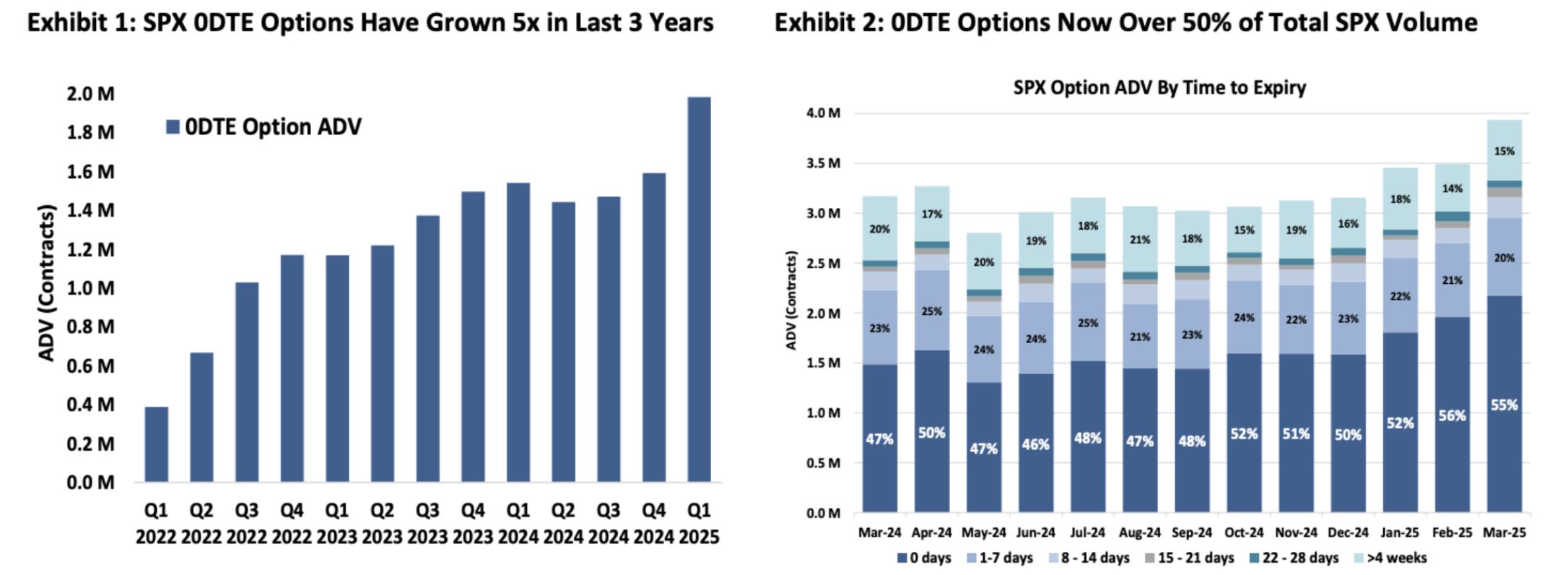

The global equity market is worth around $100 trillion — nearly 25 times larger than the entire crypto market. The US equity market alone is worth around $60 trillion. And just like in crypto, there is strong demand for leverage among equity market participants. This is evident in the explosive growth of 0DTE (zero-day-to-expiry) options, which are mostly traded by retail investors and account for over 50% of SPX options volume. Retail investors clearly want leveraged exposure to the price movements of underlying assets — a demand that perpetuals on tokenized equities could serve directly.

Source: Cboe

Source: Cboe

Perpetuals are much easier for most investors to understand than options. A product that offers 5x exposure to an underlying asset is much simpler than navigating the theta, vega, and delta of options, which require a deep understanding of options pricing models. We don’t expect perpetuals to replace the 0DTE options market, but they could capture significant market share.

As equities become tokenized, equity perpetuals could unlock a vastly larger opportunity for Ethena. We believe this makes Ethena a valuable liquidity source for bootstrapping new markets, which benefits both CEXes and DEXes, or could be captured internally by building an equity perpetuals DEX under the Ethena brand. Given the size of the equity market compared to crypto, these developments could expand the capacity of the basis trade by several orders of magnitude.

Net New Distribution from Fintechs Integrating with Decentralized Perpetuals Exchanges

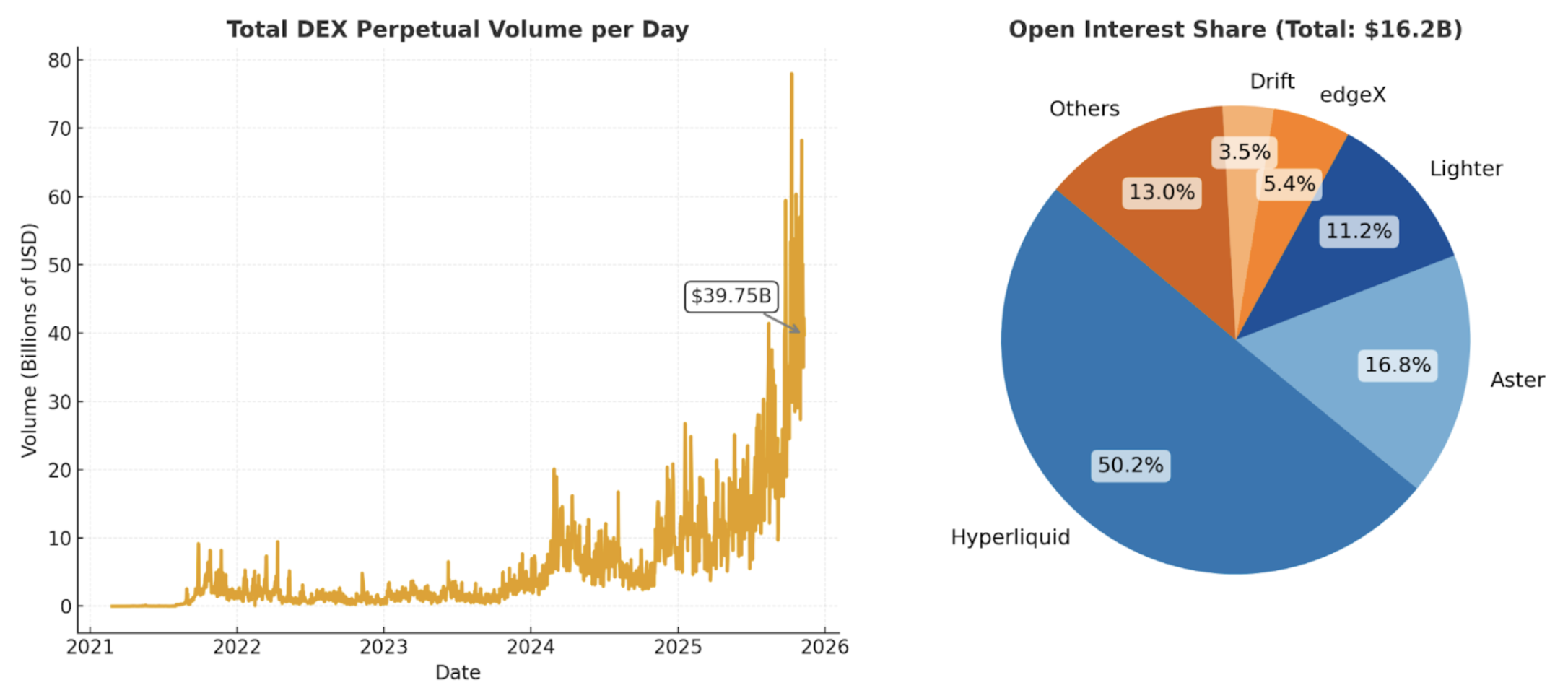

When we first published our thesis on a decentralized digital dollar backed by the basis trade, decentralized derivatives exchanges were still early — illiquid, and not yet ready for mainstream use. Since then, stablecoins have gone mainstream, and low-fee, high-throughput chains have been battle-tested. Today, platforms like Hyperliquid and others facilitate roughly $40 billion in daily decentralized perpetuals trading volume, with $15bn in open interest outstanding.

Source: DefiLlama

Source: DefiLlama

As crypto regulations turn more favorable, fintechs around the world should increasingly embrace crypto. Leading players like Robinhood and Coinbase are already evolving into “Everything Exchanges.” Many of them already integrate with DeFi middleware to enable spot trading on a long tail of assets not listed on their platform.

Today, most non-crypto-native users can only access a limited set of crypto assets, and only in spot form. We believe this group represents significant untapped demand for leverage. As decentralized perpetuals exchanges go mainstream, it’s natural to expect fintechs to integrate these products directly.

For example, Phantom recently integrated with Hyperliquid, a decentralized perpetuals exchange, allowing users to trade perps directly from their Phantom wallet. This integration added about $30 million in annualized revenue. If you are a fintech founder seeing that, it is hard not to want to follow. As an example, Robinhood recently announced their investment in Lighter, a decentralized perpetuals exchange.

We believe, as fintechs adopt crypto perpetuals, they will create a new distribution channel for these products, driving higher trading volumes and open interest, which in turn will expand the capacity and scalability of the basis trade that supports Ethena.

Tokenization

Crypto’s superpower is that it allows anyone to launch and trade tokens seamlessly. Tokens can represent anything of value, from stablecoins and L1 assets to memecoins or even tokenized strategies.

In traditional finance, the closest parallel to tokenization is the ETF. Today, there are more ETFs than publicly listed single stocks in the U.S. ETFs package complex strategies into a single, tradable ticker that investors can easily buy, sell, or hold — without worrying about execution or rebalancing. All of that complexity is handled by the ETF issuer behind the scenes. Unsurprisingly, the CEO of the world’s largest ETF issuer, BlackRock, seems to be all-in on tokenization.

Tokenization goes beyond ETFs — it makes assets faster, cheaper, and easier to own and trade in any size, while also improving distribution and capital efficiency. Anyone with an internet connection can buy, sell, send, or receive tokens instantly, and even pledge them as collateral to unlock additional liquidity. We envision a future where fintechs around the world become major distributors of tokenized strategies, bringing institutional-grade products directly to global consumers.

Ethena is starting by tokenizing the basis trade — but there’s nothing stopping Ethena from diversifying its yield sources over time. In fact, it already does this today. When the basis trade offers lower or negative returns, Ethena can shift a portion of its collateral into another product in its ecosystem USDtb, a stablecoin backed by BlackRock’s tokenized Treasury fund BUIDL, to maintain stability and optimize yield.

The Case for ENA

While we have described so far what we believe to be the long term bull case for Ethena’s addressable market size, it is also important to learn more about the team and protocol characteristics, especially when it comes to risk management, value capture and future growth opportunities.

Team

“I quit my job to build Ethena a few days after Luna collapsed and hired the team a couple of months post-FTX.” – Guy Young, the founder of Ethena.

In our experience, Guy has proven to be one of the sharpest and most strategic thinkers in DeFi, bringing his experience investing across the capital stack at Cerberus to a crypto market in the midst of rapid financialization.

Guy’s success has been supported by a lean yet experienced team of ~25 operators. To name just a few of Ethena’s team: Ethena’s CTO, Alex Nimmo, was one of BitMEX’s first employees, and was at the company during their build-out and scaling of perpetuals futures to the most important financial instrument in crypto. Ethena’s COO, Elliot Parker, worked at Paradigm Markets and Deribit, with his connections across market makers and exchanges contributing to Ethena’s success in integrations with these counterparties today.

The results speak for themselves. Ethena has become the largest synthetic dollar in less than two years. In that time, the team has moved fast, integrating with top-tier centralized exchanges and building hedging access that most projects take years to secure. USDe is now accepted as collateral on major venues like Binance and Bybit. Many of these exchanges are also investors in Ethena, showing clear strategic alignment between the protocol and key players in global crypto markets.

Risk Management

My partners Spencer and Kyle wrote an article in 2021 titled “DeFi Protocols Don’t Capture Value, DAOs Manage Risk.” The core argument was simple: DeFi protocols that do not manage risk and try to charge fees will be forked, and there will always be fee-free forks. Meanwhile, protocols that manage risk intrinsically must have fees, otherwise no one would backstop the system.

Ethena exemplifies this principle the best. The protocol has demonstrated strong risk management, successfully navigating two major stress events this year alone, each of which reinforced its credibility, resilience, and brand trust within the crypto ecosystem.

Bybit Hack: The Largest Crypto Hack To Date

Bybit’s $1.4 billion hot-wallet hack on February 21, 2025 served as a real-world stress test for Ethena’s exchange counterparty model. The incident triggered a sharp wave of user withdrawals from Bybit, yet Ethena’s strategy was unharmed.

Because hedges and collateral were diversified across multiple venues and secured in off-exchange custody, Ethena maintained normal operations throughout the event. Importantly, no Ethena collateral was lost, and there was no disruption to mint or redeem flows linked to the Bybit event.

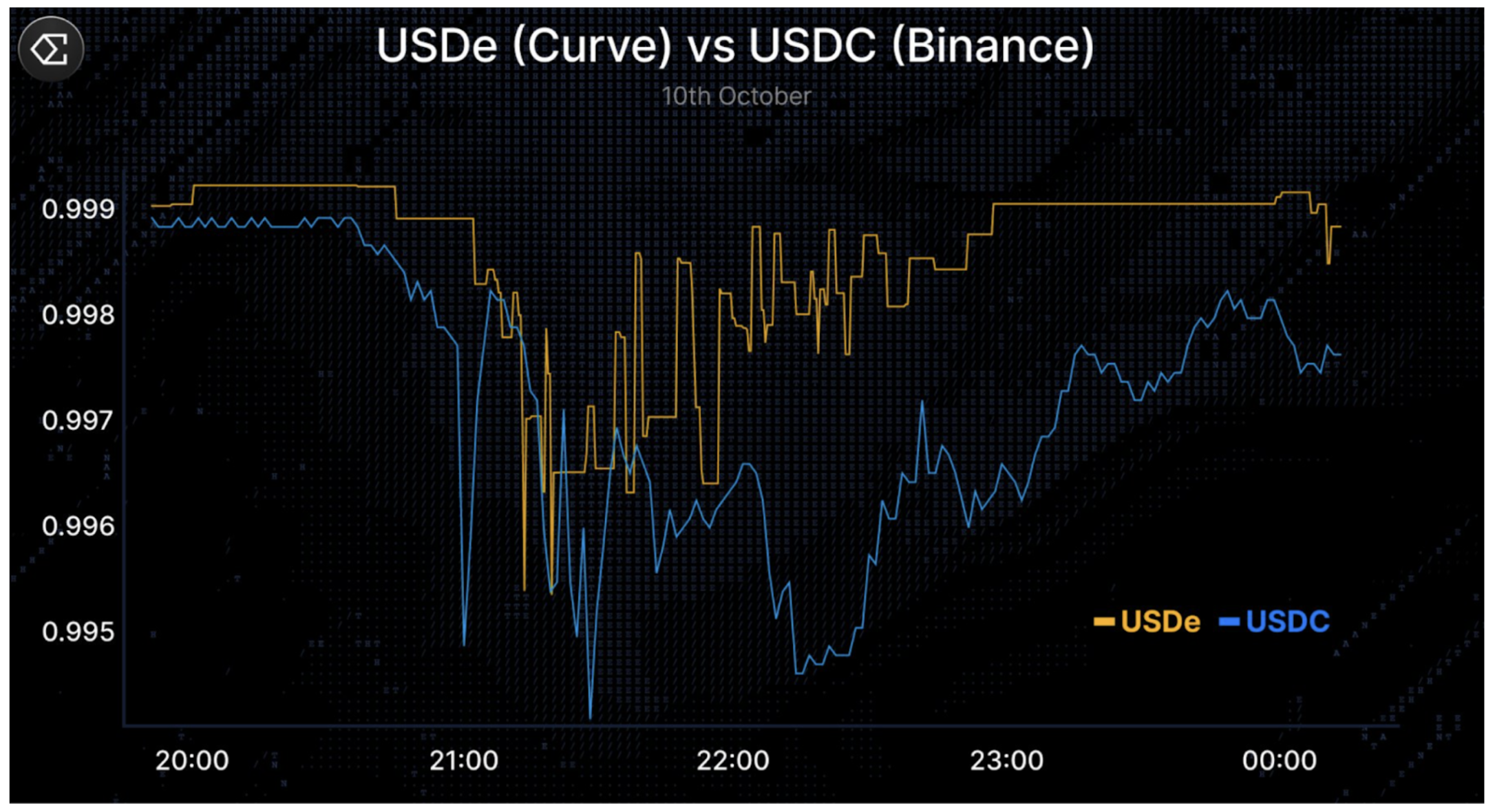

October 10 Sell-off: The Largest Single Day Liquidation Event In Crypto History

On October 10, 2025, crypto markets experienced an extreme deleveraging event, with ~$20 billion in positions liquidated within hours as open interest collapsed across major CEXes and DEXes. During the cascade, USDe briefly traded as low as ~$0.65 on Binance, a result of Binance’s oracle design, which attracted criticism. However, USDe held near parity on more liquid on-chain venues such as Curve (see below in chart), and redemptions continued to function normally — indicating a venue-specific dislocation rather than a systemic depeg. This thread on X by Guy is a great read for understanding the events of October 10.

Source: X

Source: X

In both episodes, the Ethena team communicated transparently and did not lose any user funds. Simultaneously, the protocol continued to operate as normal, facilitating 9-figures of redemptions in hours, all verifiable on chain. Moments like these test the risk discipline of any protocol. Successfully managing such stress events at scale not only reinforces trust and credibility but also builds brand equity and defensibility — building a strong moat for a DeFi protocol like Ethena.

To be clear, it’s reasonable to expect more stress tests of the Ethena protocol in the years ahead. We’re not suggesting that risk is absent or fully mitigated, but rather emphasizing that Ethena has demonstrated strong performance and resilience during some of the most significant market stress events in recent memory.

Value Capture

We believe Ethena can command a higher take rate than stablecoins like USDC. Unlike USDC, Ethena actively manages market risk, shares higher yields with users in most conditions, and is likely to be negatively correlated with interest rates in the near to medium term — all of which strengthen its ability to capture and sustain long-term value.

While the ENA token currently functions primarily as a governance token, we believe there is a clear path for it to begin accruing value. Ethena generated roughly $450 million in revenue over the past year — none of which was passed on to ENA token holders.

A fee switch proposal introduced in November 2024 outlined several milestones that needed to be met before value could flow to ENA holders. All of these conditions were met before the October 10 crash. The only metric currently below its target is USDe’s circulating supply, which we expect to exceed $10 billion before the fee switch gets activated. The risk committee and the community are now reviewing the fee-switch implementation details.

It is our assessment that these developments are likely to be viewed favorably by public markets, as they strengthen Ethena’s governance alignment, long-term holder base and reduce sell pressure on the token.

Long-Term Growth Potential

On its own, Ethena already is one of the highest revenue-generating protocols in crypto.

Ethena is leveraging its pole position to launch a number of new product lines, building on top of its core strengths of stablecoin issuance and expertise on crypto perpetuals exchanges. These product lines include:

- Ethena Whitelabel, a stablecoin-as-a-service offering where Ethena builds stablecoins for the biggest chains and applications. Ethena has already partnered with megaETH, Jupiter, Sui via SUIG among others for Ethena Whitelabel.

- HyENA and Ethereal, two third-party perpetuals DEXes built on USDe collateral, driving both USDe use cases and trading fee revenue back to the Ethena ecosystem. Both are built by external parties, but drive value directly back to Ethena.

These potential product lines can further cement Ethena’s lead in synthetic dollars.

With all net new product lines built on Ethena, Ethena should enjoy economics generated by these initiatives to sit alongside the already strong revenue numbers.

Why We Are Long Ethena

Ethena has carved out a distinct niche in the larger stablecoin market long dominated by Tether and Circle, emerging as the clear market leader in the synthetic dollar category.

As stablecoins proliferate, traditional assets become tokenized, and perpetuals DEXes take off, we believe Ethena is uniquely positioned to capture these tailwinds — transforming global demand for leverage into attractive and accessible yields for its users and fintechs around the world.

The protocol’s strong risk-management culture has been tested in real-world stress tests and has consistently delivered, helping Ethena build deep trust and credibility among its users and partners.

Over the long term, Ethena can leverage its scale, brand, and infrastructure to expand into other products, diversifying its revenue and enhancing resilience to market shocks.

As an issuer of the fastest growing synthetic dollar in the fastest growing stablecoin category— yield-bearing stablecoins—Ethena is perfectly positioned to incubate new business lines, giving it additive upside to the most profitable businesses in crypto, exchanges and on/off-ramps, all while growing USDe’s supply.

The opportunity ahead is enormous, and we’re excited as long term ENA tokenholders.

/Building The Attention Economy

Recently, crypto has instigated a new type of asset—one valued on attention. Today, “Attention Assets” are primarily user-generated assets (UGAs), like NFTs, creator coins, and memecoins.

Disclosure: Unless otherwise indicated, the views expressed in this post are solely those of the author(s) in their individual capacity and are not the views of Multicoin Capital Management, LLC or its affiliates (together with its affiliates, “Multicoin”). Certain information contained herein may have been obtained from third-party sources, including from portfolio companies of funds managed by Multicoin. Multicoin believes that the information provided is reliable and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post may contain links to third-party websites (“External Websites”). The existence of any such link does not constitute an endorsement of such websites, the content of the websites, or the operators of the websites.These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Websites. The content of such External Websites is developed and provided by others and Multicoin takes no responsibility for any content therein. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice. You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by venture funds managed by Multicoin is available here: https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced due to coordination with the development team(s) or issuer(s) on the timing and nature of public disclosure. Separately, for strategic reasons, Multicoin Capital’s hedge fund does not disclose positions in publicly traded digital assets.

This blog does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest.

Past performance does not guarantee future results. There can be no guarantee that any Multicoin investment vehicle’s investment objectives will be achieved, and the investment results may vary substantially from year to year or even from month to month. As a result, an investor could lose all or a substantial amount of its investment. Investments or products referenced in this blog may not be suitable for you or any other party. Valuations provided are based upon detailed assumptions at the time they are included in the post and such assumptions may no longer be relevant after the date of the post. Our target price or valuation and any base or bull-case scenarios which are relied upon to arrive at that target price or valuation may not be achieved.

Multicoin has established, maintains and enforces written policies and procedures reasonably designed to identify and effectively manage conflicts of interest related to its investment activities. For more important disclosures, please see the Disclosures and Terms of Use available at https://multicoin.capital/disclosures and https://multicoin.capital/terms.